New York

Tax Planner Template for New York

Plan uw federale en staatstaksen in New York in Google Sheets. Met staats-, stads- en lokale belastingen is georganiseerde planning essentieel voor inwoners van New York.

In Depth

New York's Meerlaagse Belastingrealiteit

New York heeft een progressieve inkomstenbelasting op staatsniveau met meerdere schijven die oplopen tot een van de hoogste tarieven in het land. Maar voor inwoners van New York City is het plaatje nog complexer - de stad heft zijn eigen progressieve inkomstenbelasting op boven het staatsbelastingtarief. Het gecombineerde staat-plus-gemeente tarief voor NYC inwoners op hogere inkomstensniveaus kan concurreren met de totale belastinglast in elk rechtsgebied in het land. Yonkers legt ook een gemeentelijke inkomstenbelasting toeslag op, wat nog een variatie in het grootstedelijke gebied oplevert.

De federale SALT-aftrekgrens treft inwoners van New York van meerdere kanten tegelijk. Staats inkomstenbelasting, gemeentelijke belasting (voor New York City en Yonkers inwoners) en onroerend goedbelastingen concurreren allen om dezelfde beperkte aftrek. In veel gevallen benaderen of overschrijden alleen onroerend goedbelastingen de grens, wat betekent dat de staats- en gemeentelijke inkomstenbelasting geen aanvullende federale aftrek oplevert. Dit maakt het vooral belangrijk om al deze verplichtingen op één plaats te zien bij het plannen.

New York biedt aanzienlijke bescherming van pensioeninkomen. Socialezekerheid is volledig vrijgesteld van staats belasting. Overheidspensioenen - inclusief de staat- en lokale regering van New York, federale ambtenarij en militaire pensioenen - zijn volledig vrijgesteld. Privé-pensioeninkomen ontvangt een gedeeltelijke uitsluiting voor inwoners die een bepaalde leeftijd hebben bereikt. Deze bepalingen maken het belastingplaatje voor pensioen in New York aanmerkelijk anders dan het belastingplaatje voor werkjaren, hoewel NYC pensioengerechtigden nog steeds gemeentelijke belasting op niet-vrijgesteld inkomen betalen.

New York

Belastingplanning in New York

New York heeft een progressieve inkomstenbelasting op staatsniveau met tarieven die tot de hoogste in de VS behoren, en bewoners van New York City worden geconfronteerd met een aanvullende gemeentelijke belasting. De gecombineerde belastinglast maakt grondige planning bijzonder belangrijk.

Hoge progressieve tarieven

New York heeft een progressieve inkomstenbelasting op staatsniveau met veel schijven en een toptarief van 10,9% [1]. Hogere tarieven gelden op progressief hogere inkomstendrempels, met het allereerste tarief voorbehouden aan de hoogste inkomsten.

Gemeentelijke inkomstenbelasting New York City

Bewoners van New York City betalen een aanvullende gemeentelijke belasting met hun eigen progressieve schijven, met tarieven van 3,078% tot 3,876% [2]. Gecombineerd met de staats belasting kunnen inwoners van NYC enkele van de hoogste staats- en lokale inkomstenbelastingtarieven in het land betalen.

Impact van SALT-aftrek

De federale SALT-grens is vooral van belang voor inwoners van New York, die vaak aanzienlijke staats-, gemeente- en onroerendgoedbelastingen betalen. Dit maakt federale belastingplanning cruciaal.

Pensioeninkomen

New York stelt socialezekerheidstoelagen vrij van staatsbelasting. Pensioenen van de staat- en lokale regering van New York, evenals federale overheidspensioenen, zijn volledig vrijgesteld. Een gedeelte van het inkomen uit private pensioenen is ook vrijgesteld voor inwoners boven een bepaalde leeftijd.

Haal de Jaarlijkse Belastingplanner

Aan de Slag

De Belastingplanner Gebruiken als Inwonervan New York

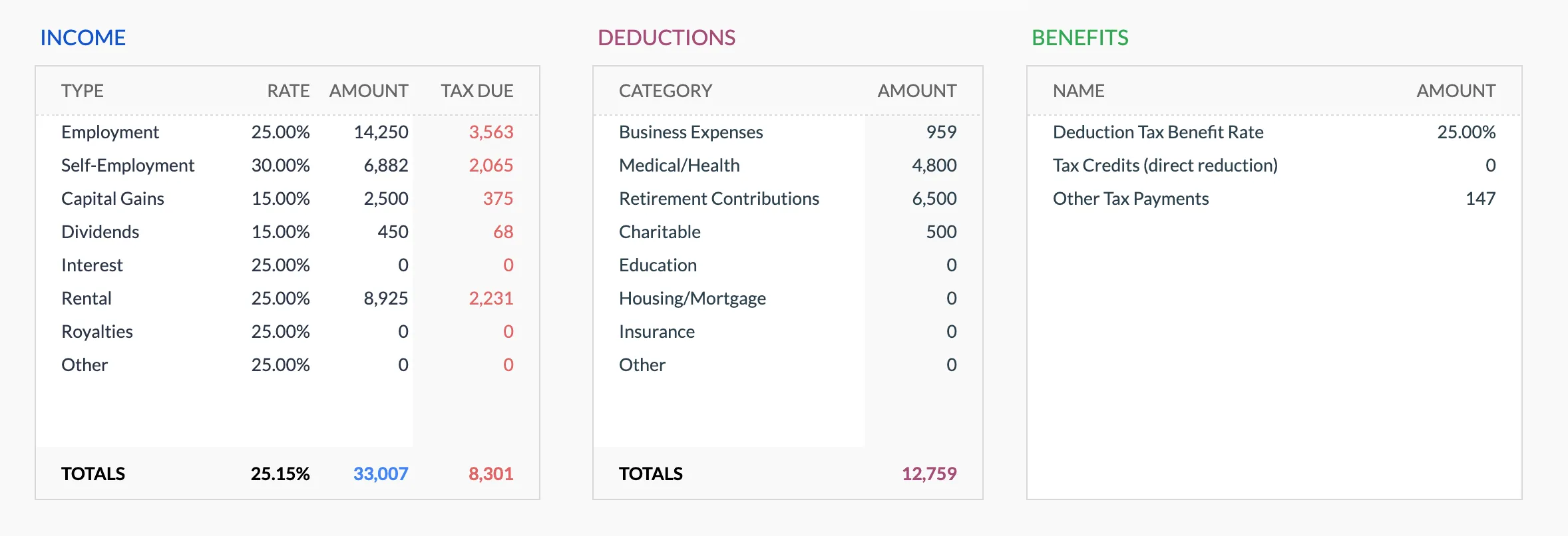

Voer inkomsten in en noteer uw locatie in New York

Voeg alle inkomstenbronnen toe - lonen, zelfstandige werk, beleggingen en ander inkomen. Uw locatie in de staat is van belang: inwoners van New York City betalen een aanvullende gemeentelijke belasting van 3,078% tot 3,876%, en inwoners van Yonkers betalen een toeslag op hun staats belasting. De MTA-mobiliteitsbelasting kan ook gelden voor zelfstandigen in het grootstedelijk gebied. Gebruik de notitie-afdeling om aan te geven welke lokale belastingen op uw situatie van toepassing zijn.

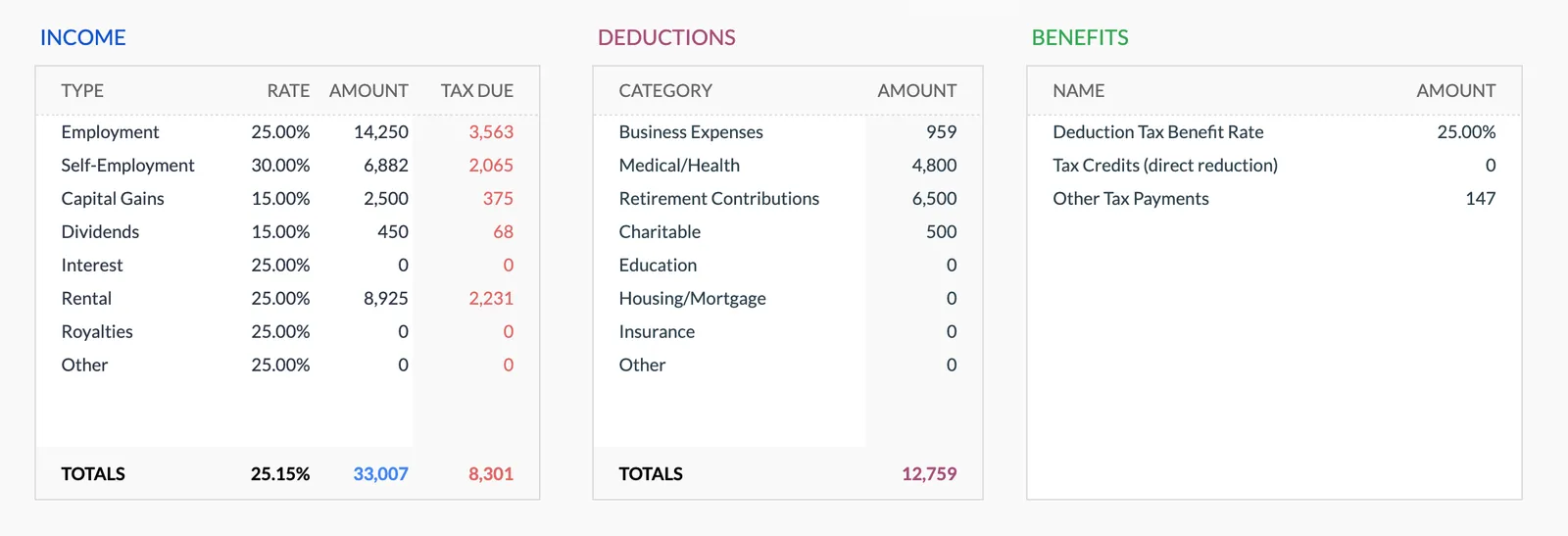

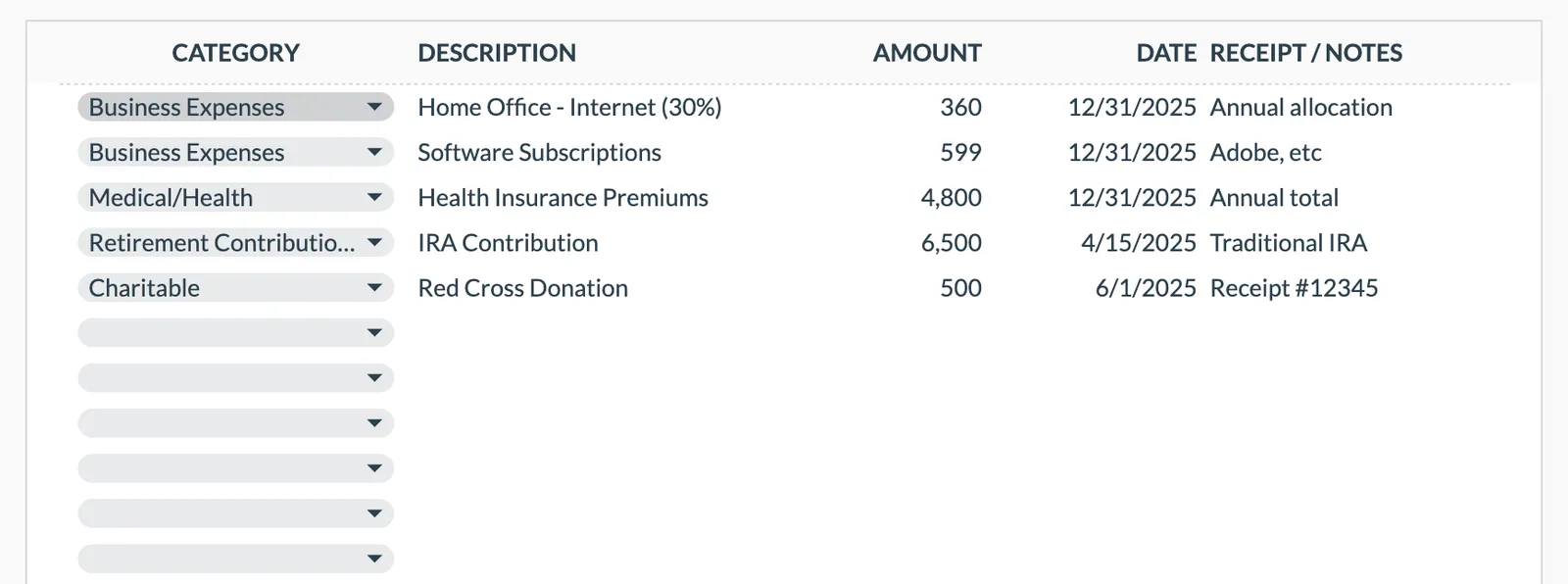

Laag staats-, gemeente- en onroerend goedbelastingen af voor het SALT-beeld

Inwoners van New York betalen vaak staats inkomstenbelasting, gemeentelijke belasting (in New York City of Yonkers) en onroerend goedbelastingen die samen ver boven de federale SALT-grens van $10.000 uitstijgen. Voer elk bedrag afzonderlijk in de aftrekken afdeling in om het gecombineerde totaal te zien en hoeveel daarvan werkelijk uw federale belastbaar inkomen vermindert. Voor veel huishoudens in New York levert het onbeperkte gedeelte geen federaal belastingvoordeel op.

Volg vrijstellingen voor overheidspensioenen indien van toepassing

New York stelt overheidspensioenen volledig vrij - staats-, gemeente- en federaal - van staats inkomstenbelasting. Privé-pensioeninkomen krijgt een gedeeltelijke uitsluiting voor inwoners die de kwalificatie leeftijd hebben bereikt. Als u pensioeninkomen ontvangt, helpt het scheiden daarvan per bron u te zien hoeveel vrijgesteld is versus belastbaar op staatsniveau. Socialezekerheid is ook volledig vrijgesteld.

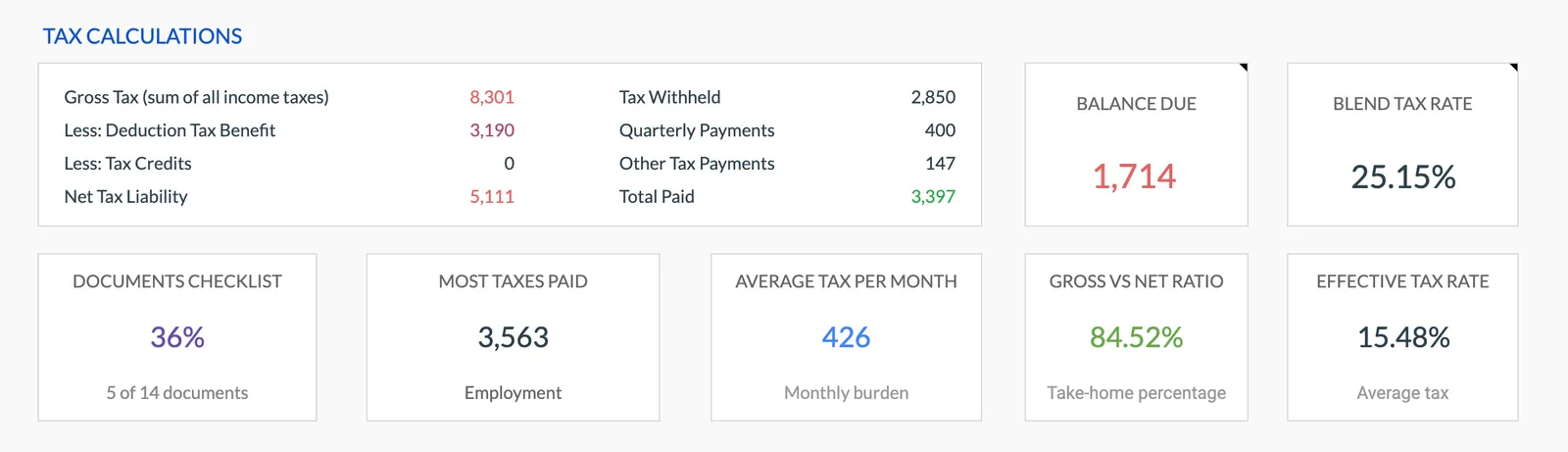

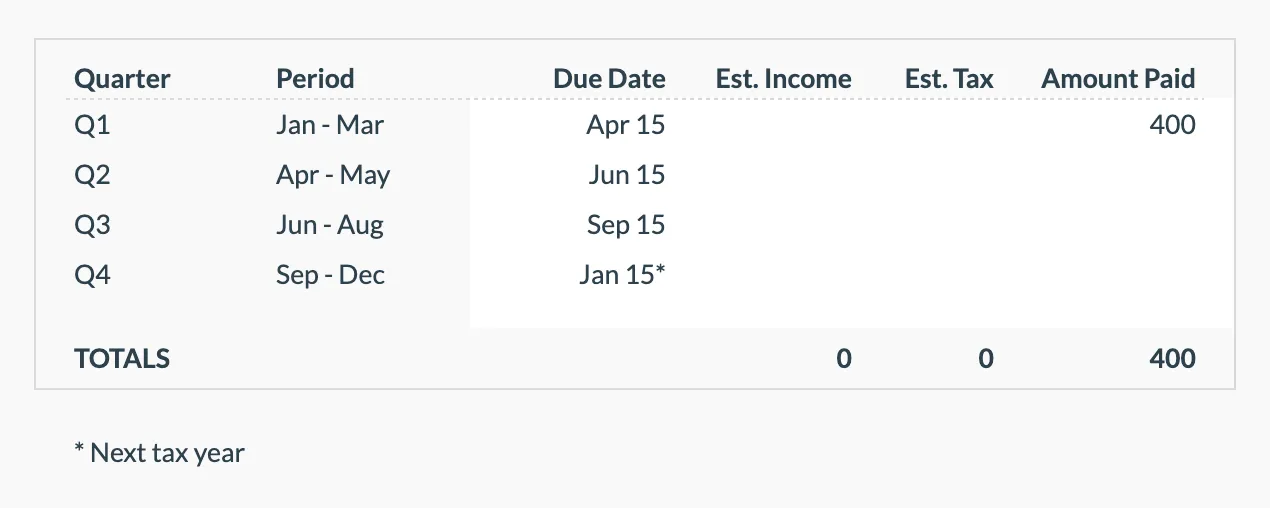

Plan geschatte betalingen in meerdere rechtsgebieden

New York State, New York City en de federale regering hebben elk hun eigen vereisten voor geschatte betalingen. Als u inkomsten hebt die niet aan bronbelasting onderhevig zijn, kunt u mogelijk driemaandelijkse schattingen aan alle drie rechtsgebieden verschuldigd zijn. Gebruik de betalingstracker om deze overlappende verplichtingen te beheren - het missen van een betaling aan een rechtsgebied brengt zijn eigen boetes met zich mee. NYC geschatte betalingen worden op hetzelfde formulier ingediend als staatschattingen.

Controleer uw gecombineerde marginale tarief

Het dashboard toont uw geraamde federale en staatstaks. Voor NYC bewoners met hogere inkomsten kan het gecombineerde marginale tarief - federaal (tot 37%) plus staats (tot 10,9%) plus gemeentelijk (tot 3,876%) - 50% overschrijden. Dit totaal op één plaats zien helpt om in perspectief te plaatsen hoe inkomensveranderingen, aftrekken of timingbeslissingen het algehele belastingplaatje beïnvloeden.

Zie het in Actie

Hoe de belastingplanner eruit ziet

Bekijk het sjabloon om te zien hoe het inkomsten, aftrekposten, kortingen en geschatte kwartaalbetalingen bijhoudt.

- Dashboard met jaarlijks belastingoverzicht

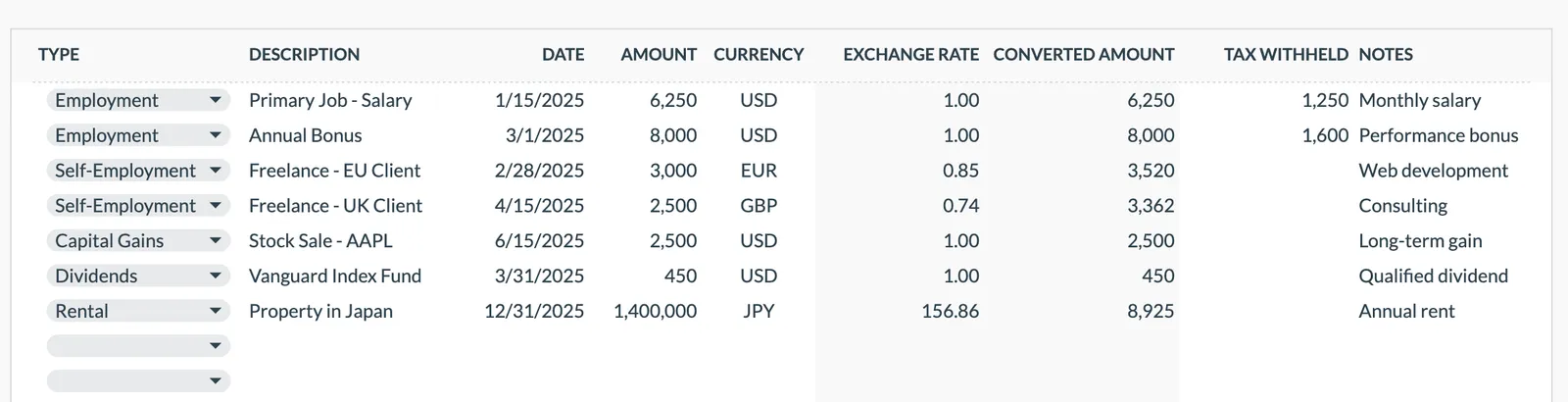

- Inkomsten bijhouden per bron

- Organisatie van aftrekposten en kortingen

- Tracker voor kwartaalbetalingen

Annual tax overview with key figures

Detailed tax breakdown and projections

Track all income sources for tax purposes

Organize and track tax deductions

Plan and track quarterly estimated tax payments

Veelgestelde Vragen

Tax Planning in New York - FAQ

Hoe werkt de gemeentelijke inkomstenbelasting van New York City boven op de staats belasting?

New York City heft zijn eigen progressieve inkomstenbelasting op met tarieven van 3,078% tot 3,876% [2], afhankelijk van inkomsten en indieningsstatus. Dit is in aanvulling op de staats belasting, die zijn eigen schijven heeft met een maximum van 10,9% [1]. Alleen inwoners van New York City betalen de gemeentelijke belasting - die in de rest van de staat niet. Yonkers heeft een aparte toeslag berekend als percentage van de staats belasting. Het gecombineerde staat-plus-gemeente tarief voor NYC bewoners met hogere inkomsten is een van de hoogste in elk rechtsgebied in het land.

Wat is de MTA-toeslag en wie betaalt deze?

De mobiliteitsbelasting van de Metropolitan Transportation Authority (MTA) is van toepassing op zelfstandigen die boven bepaalde drempels verdienen in het MTA pendel district - dat New York City en verschillende omringende counties omvat. De belasting is een percentage van de netto inkomsten uit zelfstandig werk. Het staat los van zowel de staats- als de gemeentelijke inkomstenbelasting. Werknemers betalen deze belasting niet rechtstreeks, hoewel werkgevers in het district een gerelateerde loonbelasting betalen.

Hoe beïnvloedt de SALT-grens inwoners van New York?

De federale SALT-grens van $10.000 is vooral belangrijk in New York omdat inwoners vaak staats inkomstenbelasting, gemeentelijke belasting (in New York City) en hoge onroerend goedbelastingen betalen. Deze drie bedragen kunnen samen gemakkelijk $10.000 overschrijden - soms met een groot veelvoud. Aangezien slechts $10.000 in totaal aftrekbaar is op de federale aangifte, levert een aanzienlijk deel van de staats- en lokale belastingen geen federaal belastingvoordeel op. Dit maakt het bijzonder nuttig voor inwoners van New York om het volledige beeld op alle niveaus bij te houden.

Heft New York belasting op pensioeninkomen?

Socialezekerheid is volledig vrijgesteld van de inkomstenbelasting van New York State. Overheidspensioenen - inclusief de staat- en lokale regering van New York, federale ambtenarij en militaire pensioenen - zijn ook volledig vrijgesteld ongeacht het bedrag. Privé-pensioeninkomen komt in aanmerking voor een gedeeltelijke uitsluiting (momenteel $20.000 per persoon) voor inwoners die de kwalificatie leeftijd hebben bereikt. Ander pensioeninkomen zoals 401(k) en IRA distributies zijn doorgaans belastbaar tegen normale staatstariefen. NYC bewoners verschuldigd ook gemeentelijke belasting op belastbaar pensioeninkomen.

Wat gebeurt er als ik gedurende het jaar uit New York vertrek?

New York staat bekend om nauwkeurig woonplaatsaanspraken te beoordelen. Als u halverwege het jaar vertrekt, dient u in als deeltijd inwonersstatus en bent u staats inkomstenbelasting verschuldigd over inkomsten die u verdient heeft als inwoner, plus New York-bron inkomsten die u na uw vertrek hebt verdiend. New York controleert voormalige inwoners die beweren te zijn verhuisd - vooral naar staten zonder inkomstenbelasting - en onderzoekt factoren zoals waar u een huis onderhoudt, waar uw familie woont en hoeveel dagen u in de staat hebt doorgebracht. Gedetailleerde documenten van uw verhuizing en nieuwe woonplaats onderhouden is de moeite waard.

Can't find the answer you're looking for? Contact our team

Officiële belastingbronnen

Voor actuele tarieven, formulieren en aangiftedeadlines specifiek voor New York:

Sources

Organize your tax planning for New York

Eenmalige aankoop. Geen abonnement. Uw financiële gegevens blijven in uw Google Drive.