Life Event Guide

Financial Planning When Getting Married

Getting married affects taxes, insurance, estate planning, and daily spending all at once. Couples who combine or coordinate finances early - tracking joint income, shared expenses, and individual spending - tend to avoid the money conflicts that strain roughly 35% of marriages.

In Depth

Money and Marriage - The Conversation Most Couples Skip

Financial compatibility is not about having the same income or identical spending habits. It is about having shared visibility into the numbers and a framework for making decisions together. Couples who openly discuss their finances before and during marriage tend to experience less financial stress - not because they have more money, but because there are fewer surprises.

The merging of financial lives rarely happens all at once. Some couples combine everything on day one, while others take years to fully integrate. There is no evidence that one approach produces better outcomes than another. What does seem to matter is that both partners understand the full household picture, even if they manage day-to-day money differently.

Wedding spending is an interesting early test of how a couple navigates financial decisions together. The average wedding costs around $30,000 [1], and the process of choosing between a larger wedding and a larger savings account often reveals each person's deeper values around money. Some couples discover misalignments during this process that are worth addressing early.

One pattern that financial therapists frequently observe is that money conflicts in marriage are rarely about money itself. Disagreements about spending often reflect differences in values, risk tolerance, or childhood experiences with money. Recognizing this can shift the conversation from "you spent too much" to "we see this differently, and here is why."

Financial Impact

The Financial Impact of Getting Married

Marriage changes your financial landscape in ways that go far beyond the wedding day. Two incomes, two sets of debts, and two different spending habits need to come together into something that works for both people.

Wedding costs can reshape your savings

The average wedding in the U.S. costs around $30,000 [1], though many couples spend anywhere from $10,000 to $50,000+. Even with family contributions, this can significantly reduce savings or add debt. Tracking every vendor payment, deposit, and tip in a spreadsheet helps prevent overspending - and some couples find that seeing the total in one place naturally encourages more thoughtful choices.

Combined income changes your tax picture

Filing jointly can result in lower taxes for couples with one higher earner - or a "marriage penalty" when both earn similar amounts. The difference can be $2,000-$5,000 per year in either direction. Running the numbers for both filing jointly and separately (where applicable) is worth doing before the first tax season as a married couple.

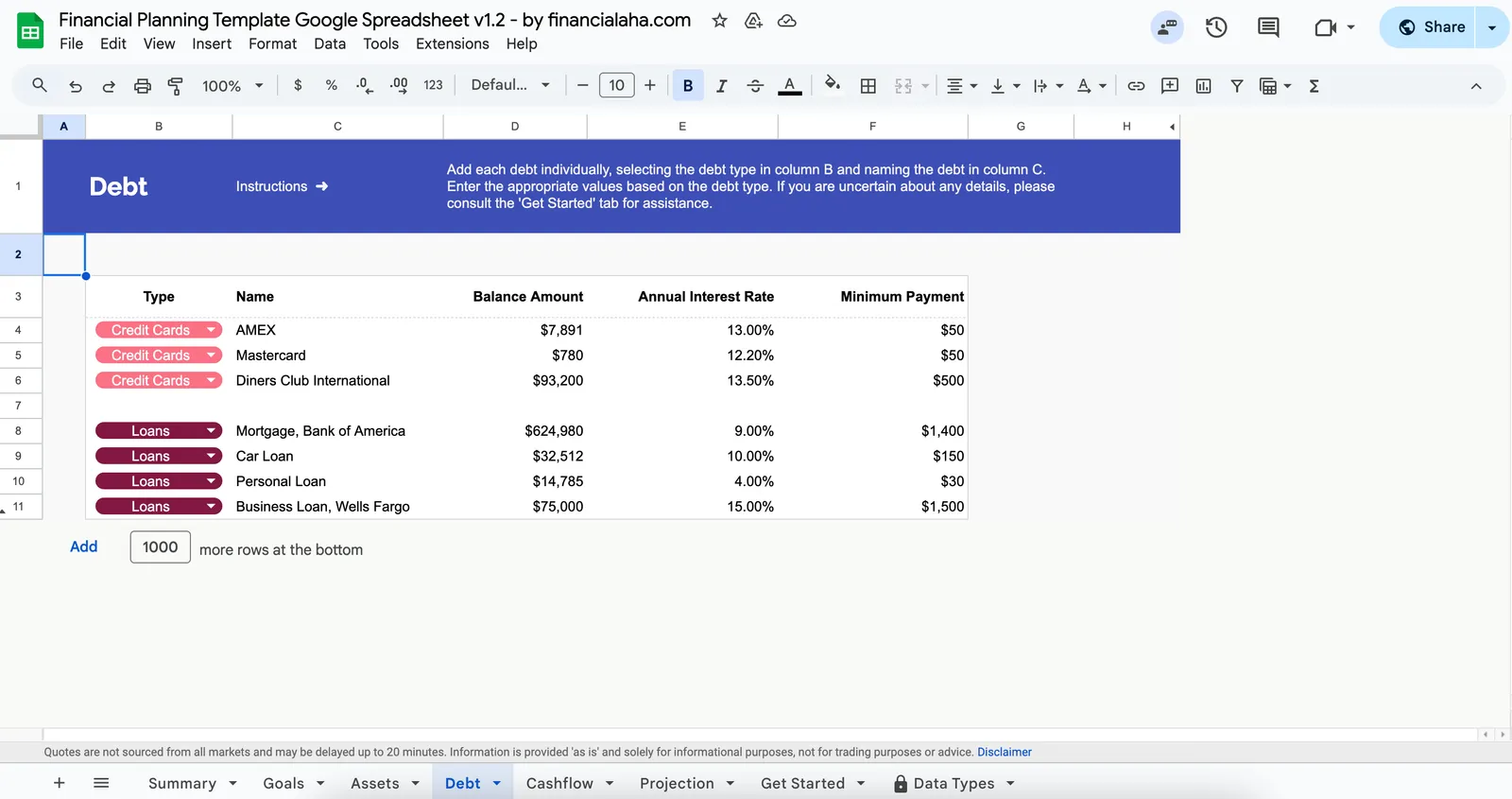

Debt becomes a shared concern

While pre-marital debt legally stays with the individual in most states, it affects household cash flow either way. If one partner carries $40,000 in student loans with $400/month payments, that is $400 less available for shared goals. Having an honest conversation about all debts - amounts, interest rates, and minimum payments - is a useful starting point.

Insurance and benefits may change

Combining health insurance onto one plan can save $1,200-$3,600 per year compared to two separate plans. Beneficiary designations on retirement accounts and life insurance policies need updating. Some employer benefits like HSA contribution limits or dependent care FSAs also change with marital status.

Getting Ready

How to Prepare Your Budget for Marriage

Have the full financial disclosure conversation

Before combining anything, lay out the complete picture: income, savings, debts, credit scores, and spending habits. Some couples use a shared spreadsheet for this - listing every account, balance, and monthly obligation. This is not about judgment; it is about having accurate data to plan with.

Decide on a money management structure

Common approaches include fully combined finances, completely separate accounts, or a hybrid with a joint account for shared expenses and individual accounts for personal spending. There is no single correct answer - the hybrid approach works well for many couples, with each contributing a proportional amount (based on income) to the joint account.

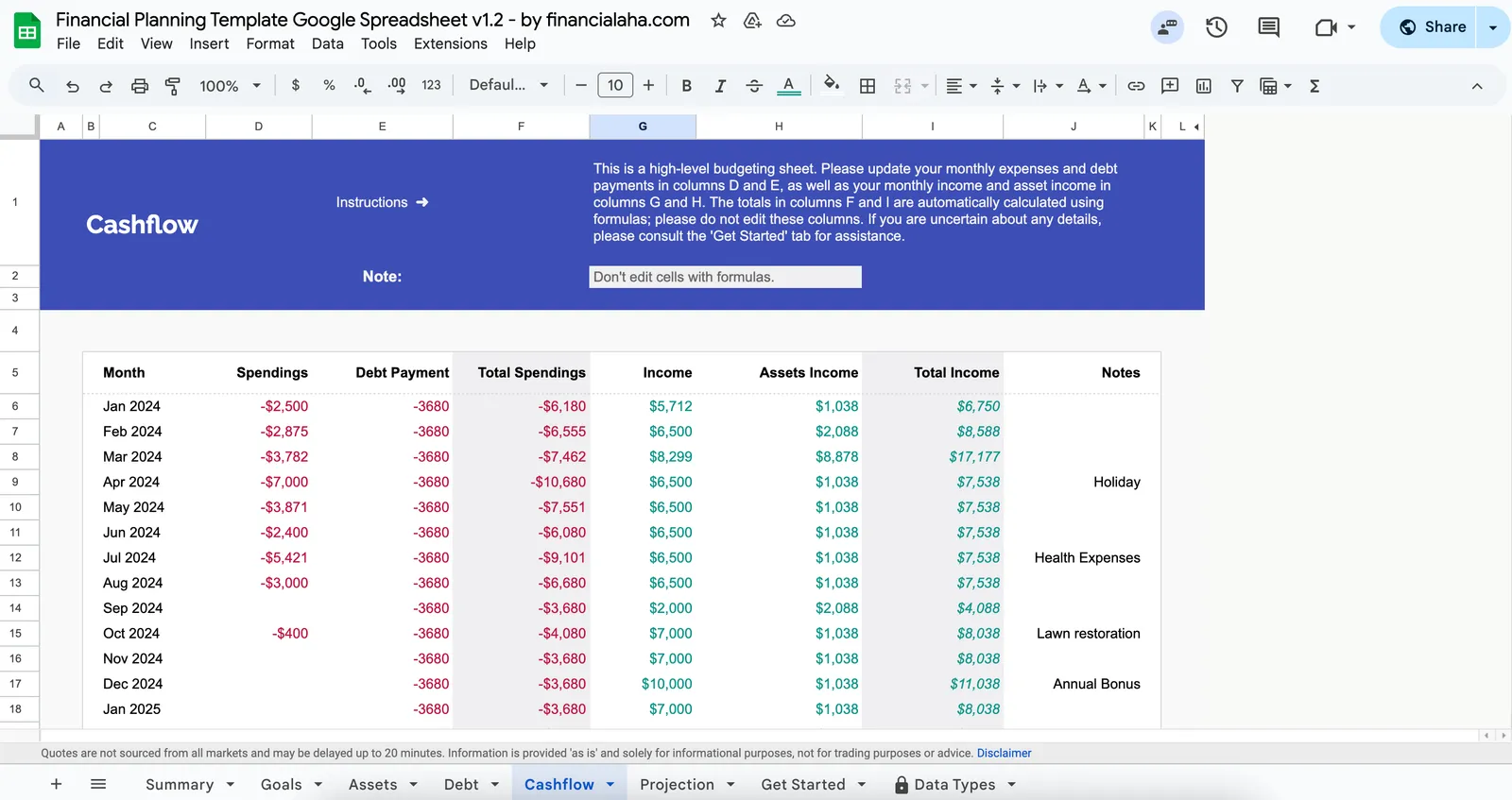

Create a combined monthly budget

Map out all shared expenses: housing, utilities, groceries, insurance, subscriptions, and debt payments. Then add individual categories. A combined household income of $120,000 looks different when you factor in $2,400 in rent, $800 in student loan payments, and $600 in car payments. Seeing it all in one budget reveals how much is actually available for savings and discretionary spending.

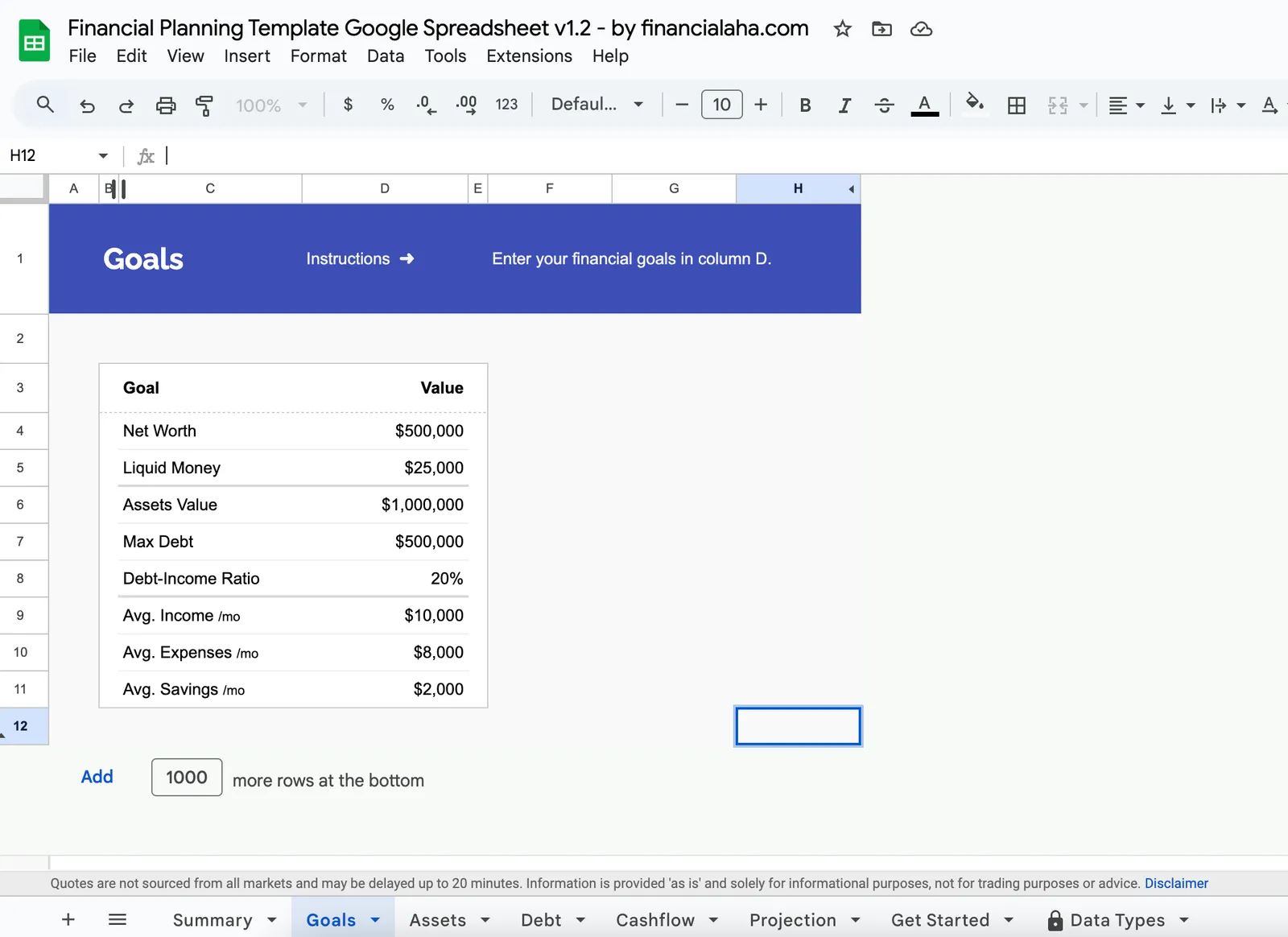

Set shared financial goals

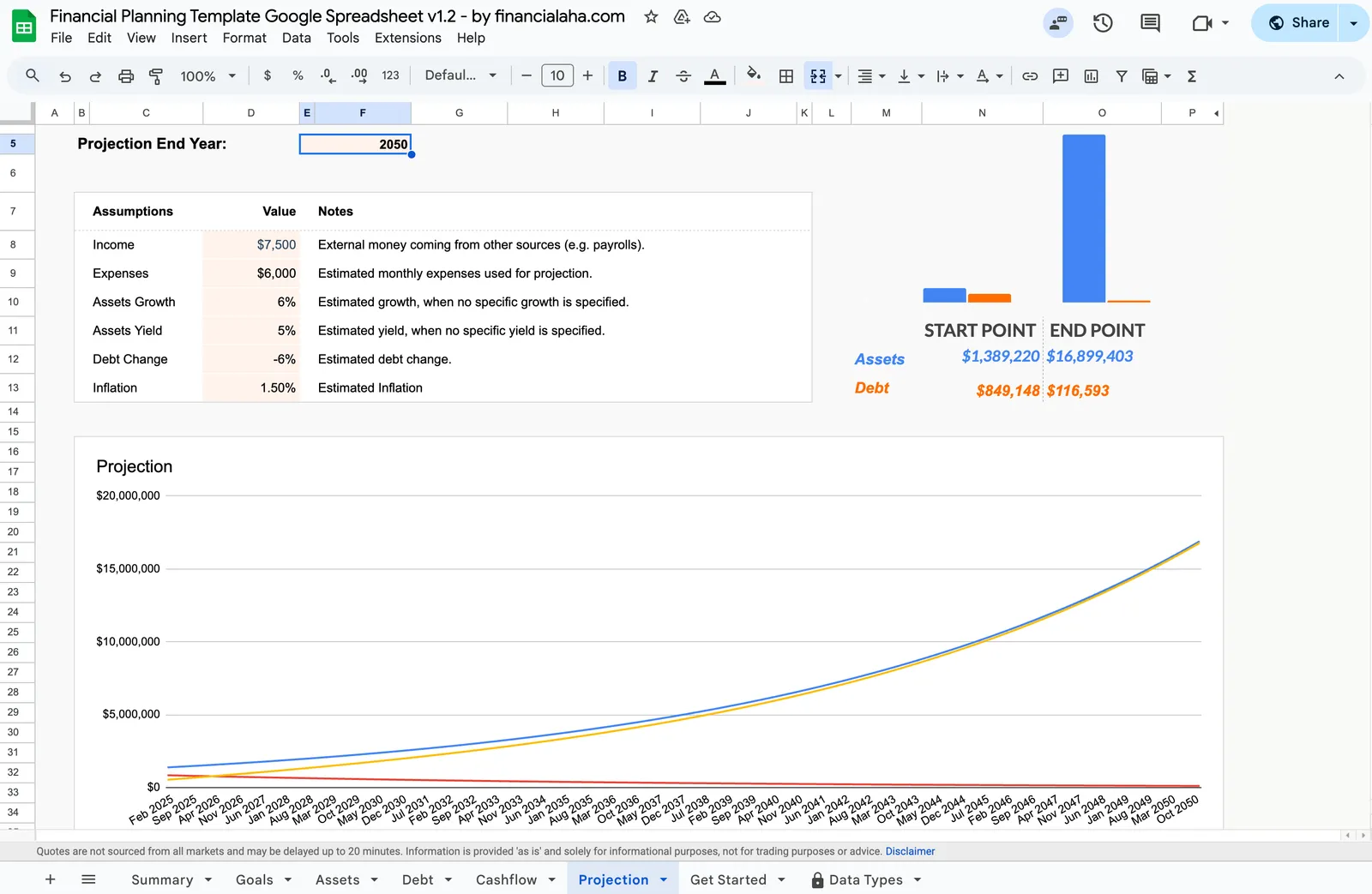

Agree on 2-3 priorities for the first year: building an emergency fund, paying off high-interest debt, or saving for a home. Having shared goals prevents the "your spending vs. my spending" dynamic. Track progress together monthly - even a quick 15-minute check-in keeps both partners engaged.

Update your legal and financial documents

Update beneficiaries on retirement accounts, review life insurance needs, consider estate planning basics like wills and power of attorney. These are not exciting tasks, but they matter. A checklist in your financial planning spreadsheet can track what has been completed and what still needs attention.

See The Templates

Tools for this stage of life

Browse the templates that help with financial planning during major life transitions.

- Financial planning dashboard

- Monthly budget tracking

- Net worth over time

- Goal setting and tracking

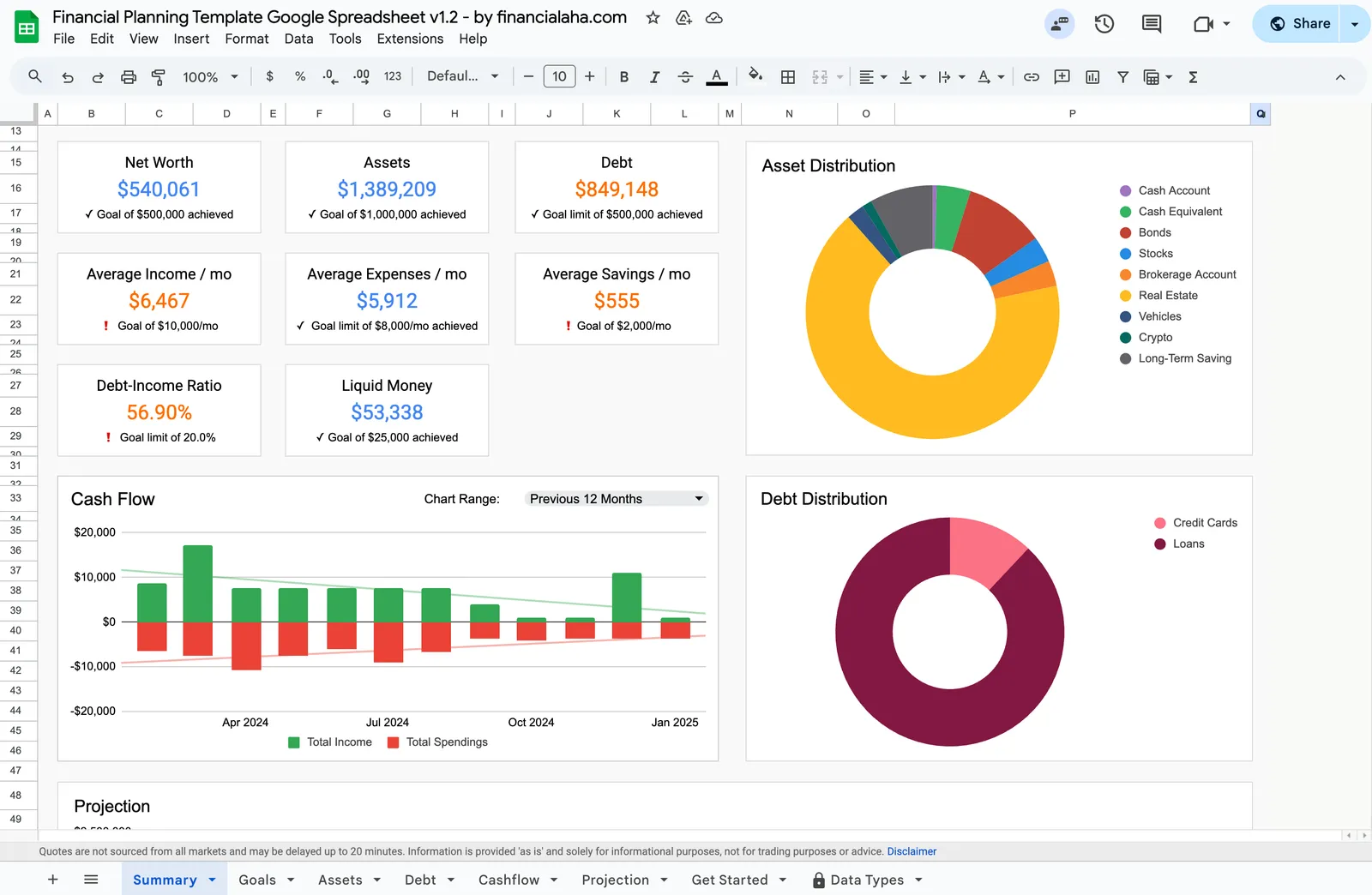

Complete financial overview with net worth and goals

Set and track progress toward financial milestones

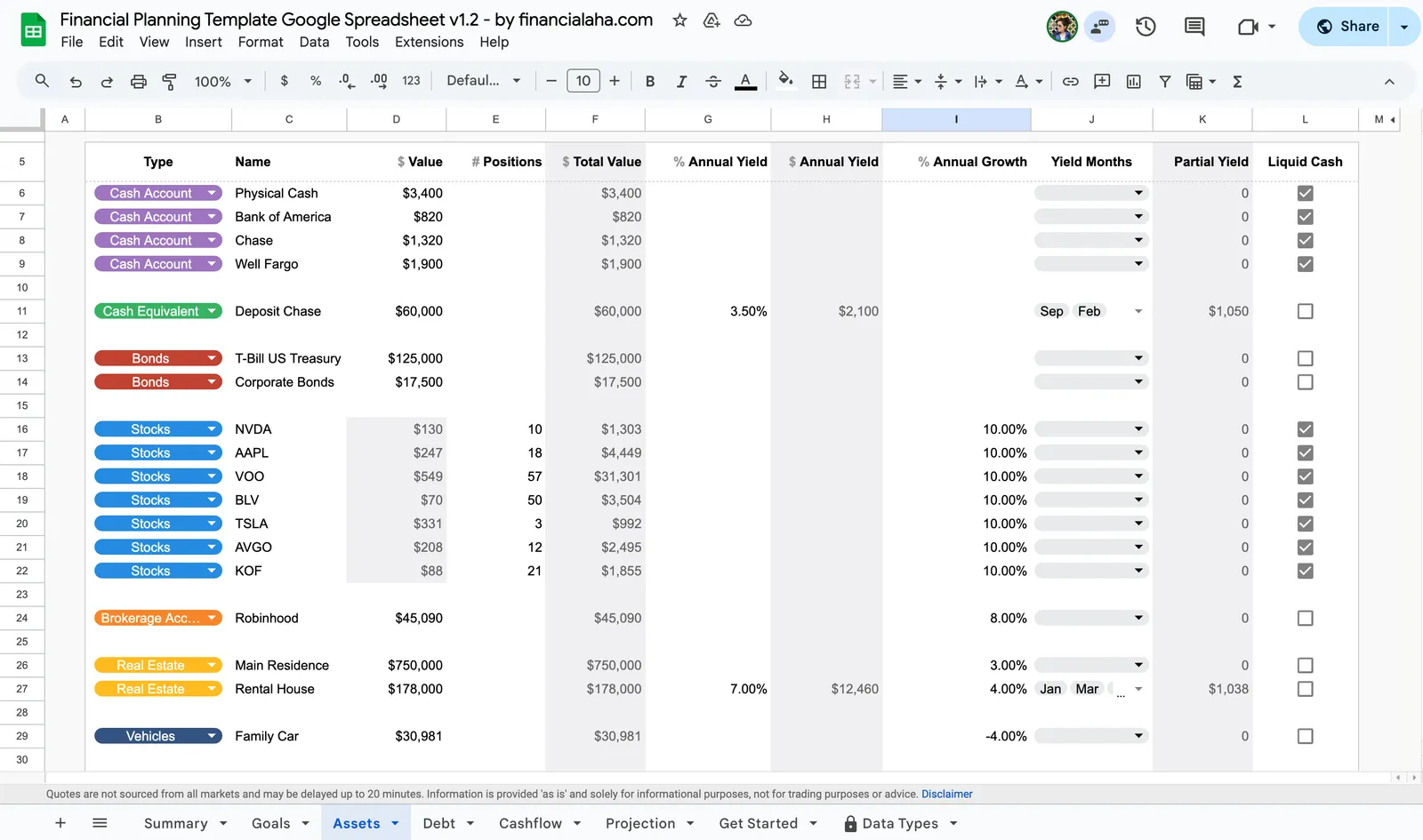

Track all your assets in one place

Monitor and plan debt repayment

Visualize your income vs spending over time

Project your financial future

Recommended Templates

Financial Tools for the Newly Married

Marriage is a financial merger. These templates help couples see the combined picture clearly:

Build your first combined household budget. Track shared and individual expenses, see where money goes each month, and adjust categories as you learn each other's spending patterns.

View templateMap out your combined financial picture - from wedding savings goals to long-term plans. Particularly useful for modeling different scenarios like home purchases or career changes.

View templateSee the full picture of combined assets and liabilities. Watching your joint net worth grow month over month can be motivating, especially in the early years of building together.

View templateFree Tools

Calculators to Help You Plan

Common Questions

Getting Married - Financial FAQ

How do couples typically split shared expenses?

Three common approaches: 50/50 split regardless of income, proportional split based on income (if one earns 60% of household income, they cover 60% of shared costs), or fully combined where all income goes into one pool. The proportional approach tends to feel fairest when there is a significant income gap.

Is it worth combining all finances after marriage?

This is a personal decision with no universally correct answer. Some couples find full combination simpler and more transparent. Others prefer the autonomy of separate "fun money" accounts. The hybrid approach - a joint account for shared expenses plus individual accounts - offers a middle ground that many couples find works well.

How much does a wedding budget typically affect long-term finances?

A $30,000 wedding paid in cash delays other goals by the time it takes to rebuild that savings. If financed on credit cards at 20% interest, the true cost can reach $40,000+ over several years. Some couples find that a smaller wedding and a larger down payment fund better serves their long-term goals - but this is a deeply personal choice.

What financial documents need updating after marriage?

Key updates include: retirement account beneficiaries, life insurance beneficiaries, health insurance enrollment, tax withholding (W-4 forms), estate planning documents (wills, power of attorney), and bank account ownership if combining. A tracking checklist helps ensure nothing falls through the cracks.

Can't find the answer you're looking for? Contact our team

Ready to get started?

Download instantly and start managing your finances, or contact us to design a custom template package for your needs.