Life Event Guide

Financial Planning When Starting a Business

From startup costs to cash flow forecasting - understanding the financial side of launching a business helps founders make informed decisions about timing, funding, and growth.

Financial Impact

The Financial Impact of Starting a Business

Starting a business introduces a level of financial complexity that surprises many first-time founders. Personal and business finances become intertwined, income becomes irregular, and the gap between launching and profitability can stretch longer than expected.

Startup costs vary wildly by business type

A freelance consulting business might launch for $500-$2,000 (website, business cards, accounting software). A physical retail store can require $50,000-$150,000+ (lease deposits, inventory, fixtures, permits). Online businesses typically fall in between at $2,000-$20,000 (website development, marketing, tools, inventory if applicable). Documenting every expense from day one matters for tax deductions and understanding true startup costs.

The profitability timeline is usually longer than planned

Most small businesses take 2-3 years to become consistently profitable. This means personal savings or alternative income need to cover both living expenses and business shortfalls during this period. A service business with low overhead might break even in 6-12 months, while a product business with inventory and marketing costs often takes 18-36 months.

Self-employment taxes add a significant cost layer

As an employee, you pay 7.65% in FICA taxes while your employer matches it. As self-employed, you pay both halves - 15.3% on top of income tax. On $80,000 in business income, that is roughly $12,240 in self-employment tax alone, before federal and state income taxes. Quarterly estimated tax payments are required to avoid penalties.

Personal financial stability affects business decisions

Founders with 6-12 months of personal living expenses saved make different (often better) business decisions than those under immediate financial pressure. The ability to say no to a bad client, invest in marketing, or wait for the right opportunity depends on personal financial stability. Some founders maintain part-time employment during the early stages for this reason.

Getting Ready

How to Prepare Your Finances for Starting a Business

Separate personal and business finances from day one

Open a dedicated business bank account and business credit card before the first transaction. Commingling funds creates accounting headaches, tax complications, and can pierce the liability protection of an LLC or corporation. Even sole proprietors benefit from clear separation - it makes tax time dramatically simpler.

Build a personal financial runway

Before launching, accumulate 6-12 months of personal living expenses in savings. If your monthly personal costs are $4,000, that means $24,000-$48,000 set aside specifically for living expenses. This is separate from business capital. Having this runway reduces the pressure to take every project or undercharge for services just to pay rent.

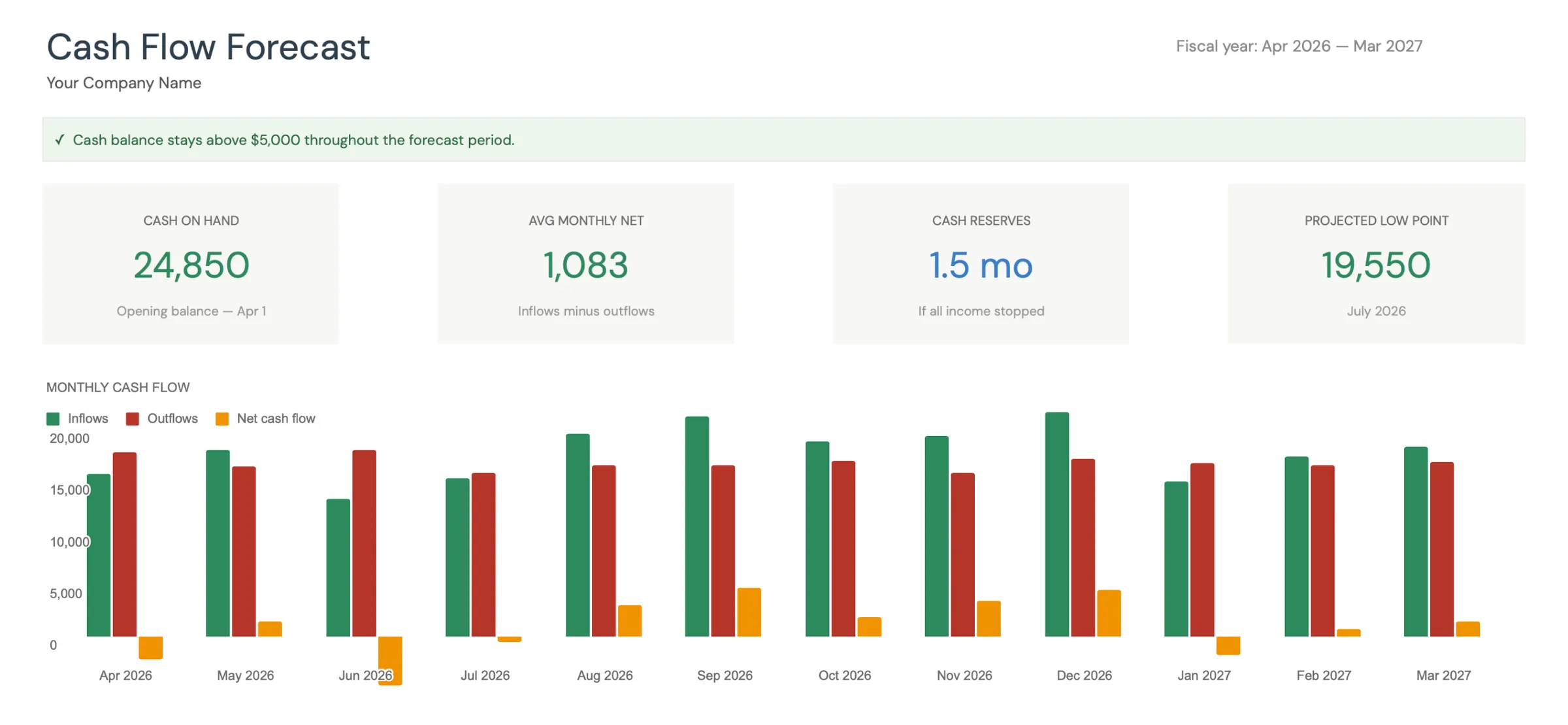

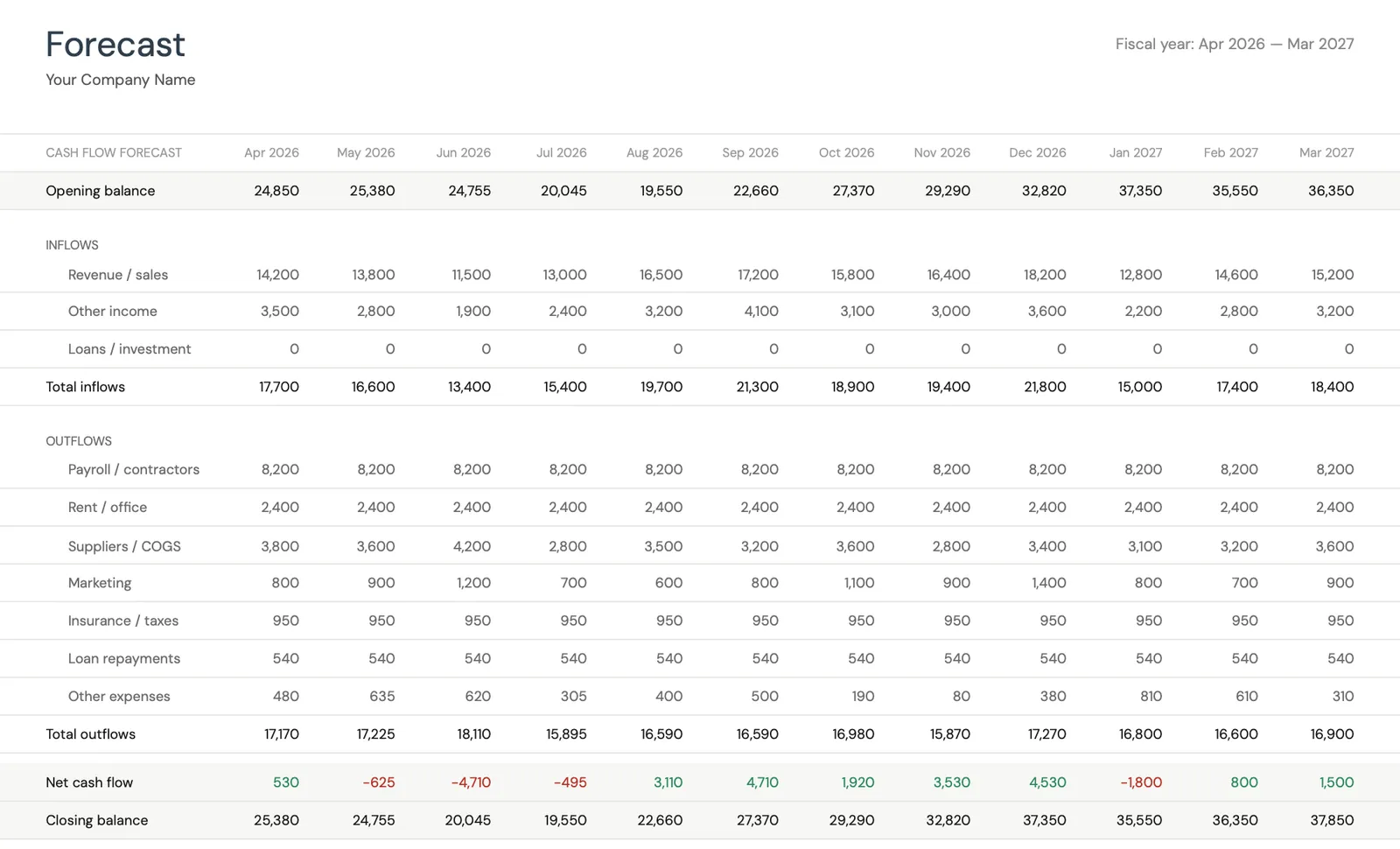

Create a cash flow forecast for the first 12 months

Project monthly revenue (conservatively - cut your optimistic estimate in half), then list all expected expenses: rent, tools/software, marketing, insurance, professional services (accountant, lawyer), inventory, and contractor costs. Most businesses are cash-flow negative for the first several months. Knowing when you expect to break even helps plan funding needs.

Plan for taxes as a self-employed individual

Set aside 25-30% of every payment received for taxes. Self-employment tax (15.3%) plus federal and state income taxes add up quickly. Quarterly estimated tax payments are due in April, June, September, and January. Missing these triggers penalties. An annual tax planner helps track income, expenses, and estimated tax obligations throughout the year.

Track every business expense meticulously

Business expenses reduce taxable income - but only if documented. Home office deduction, vehicle use, equipment, software subscriptions, professional development, and business meals all qualify. A missed $500 deduction at a 30% effective tax rate costs $150 in unnecessary taxes. Tracking from day one is far easier than reconstructing records at year end.

See The Templates

Tools for this stage of life

Browse the templates that help with financial planning during major life transitions.

- Financial planning dashboard

- Monthly budget tracking

- Net worth over time

- Goal setting and tracking

Visual dashboard with cash flow projections and trends

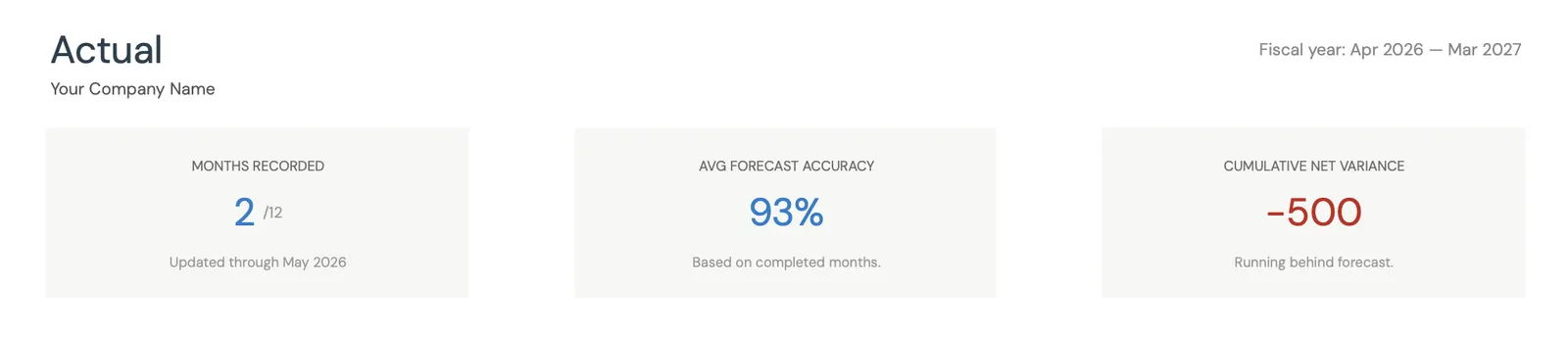

Monthly cash flow forecast with income and expenses

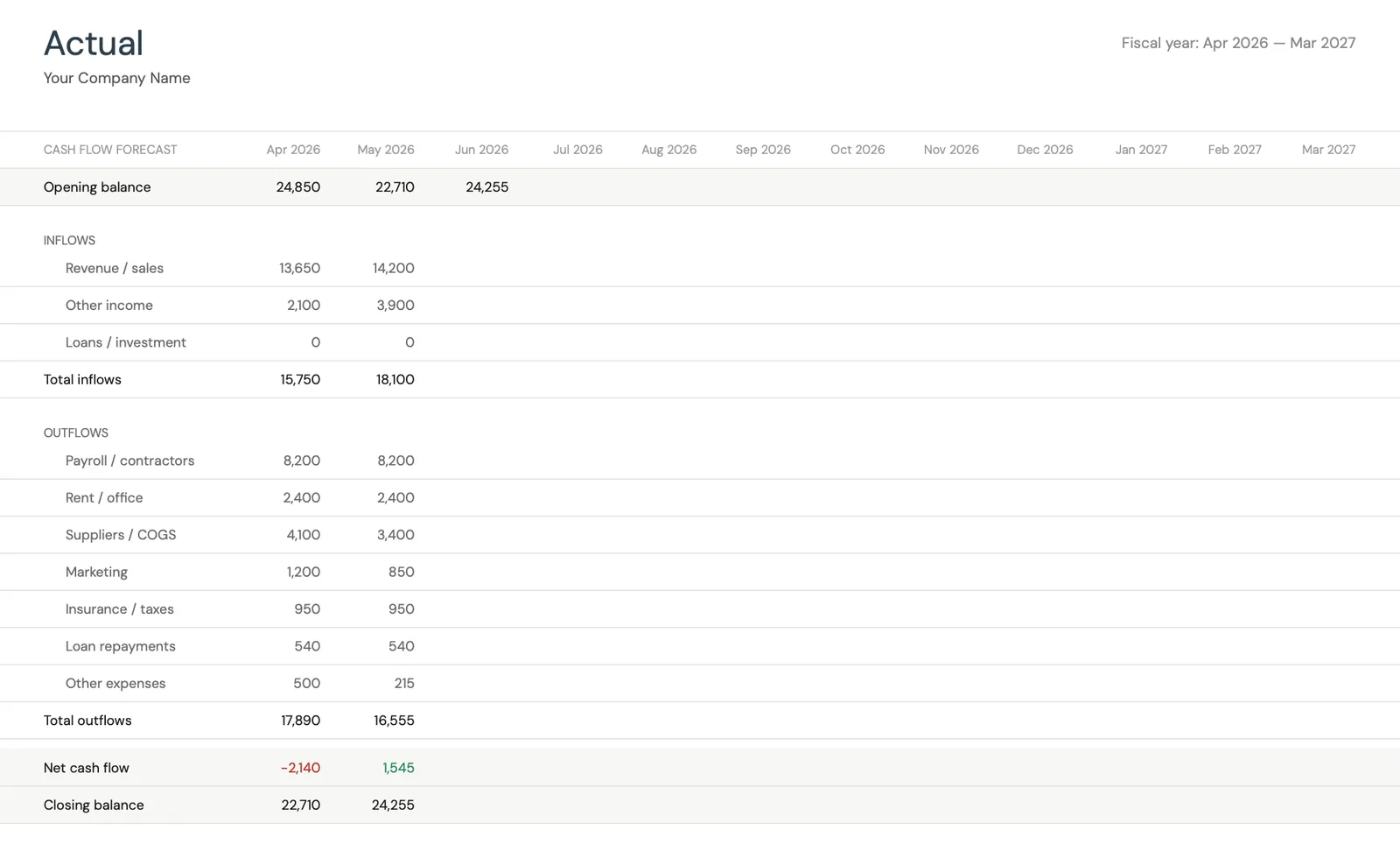

Track actual cash flow against your forecast

Key performance indicators for your cash flow

Monitor closing balances over time

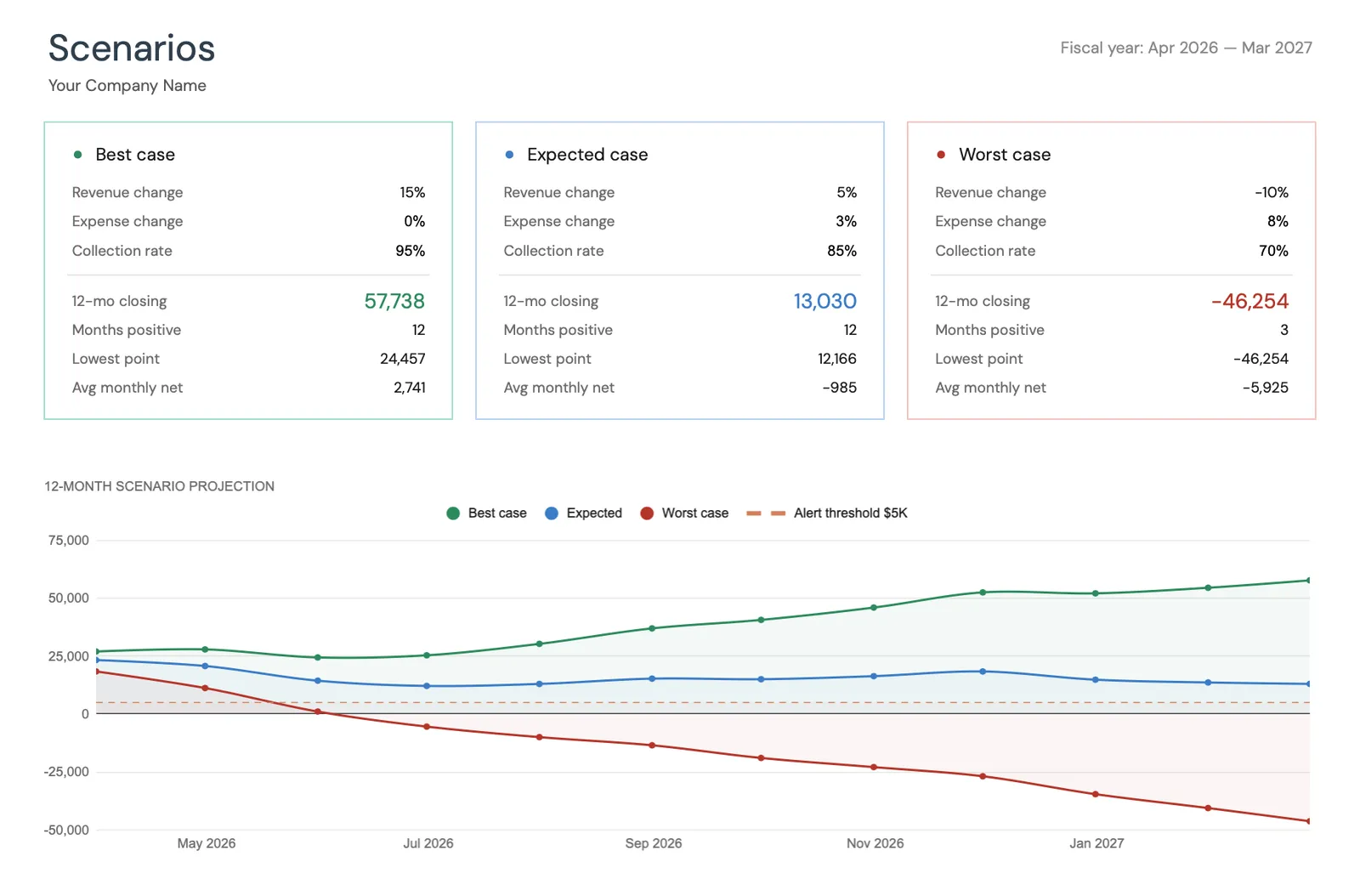

Model different business scenarios and their impact

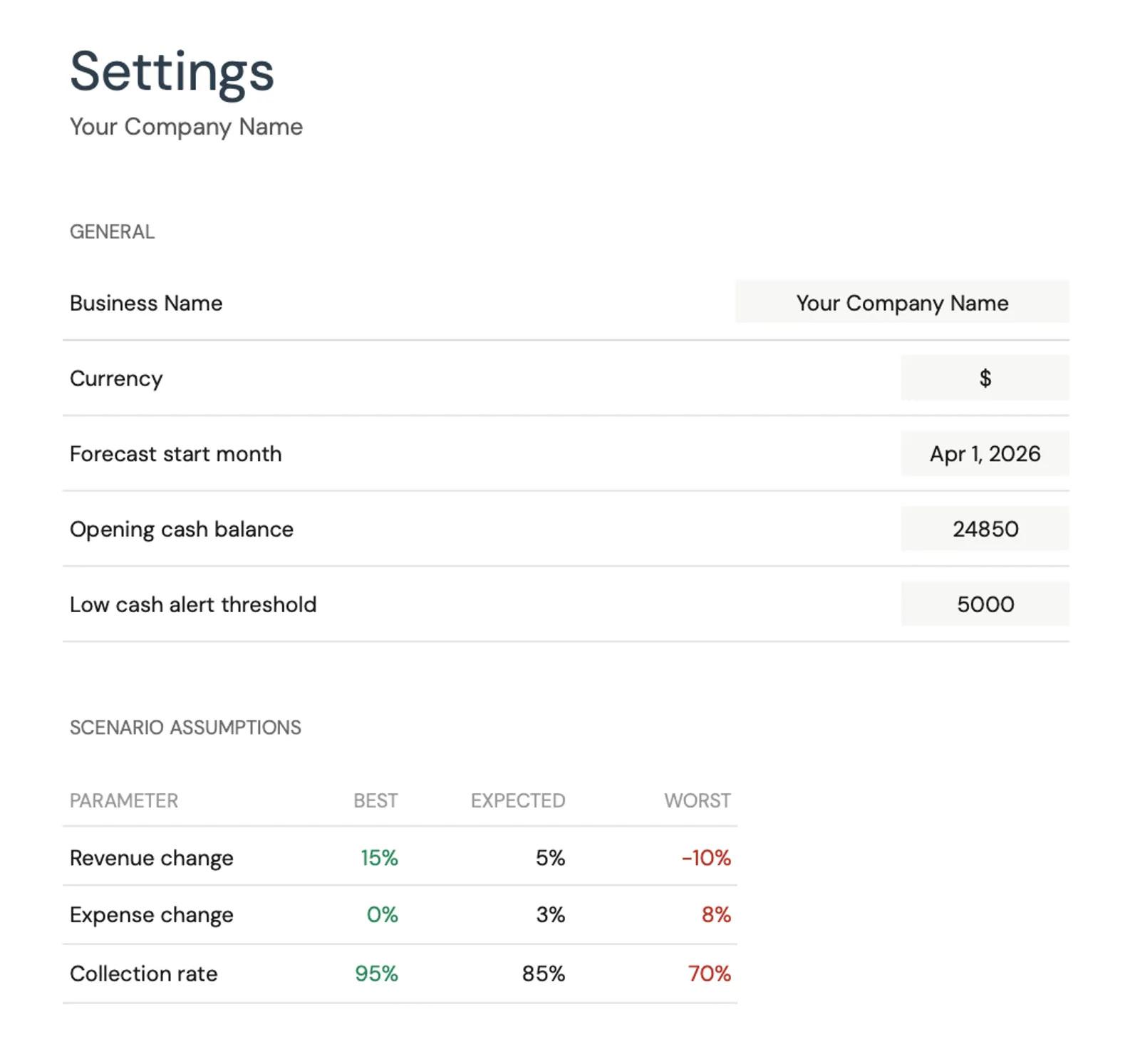

Configure income categories and settings

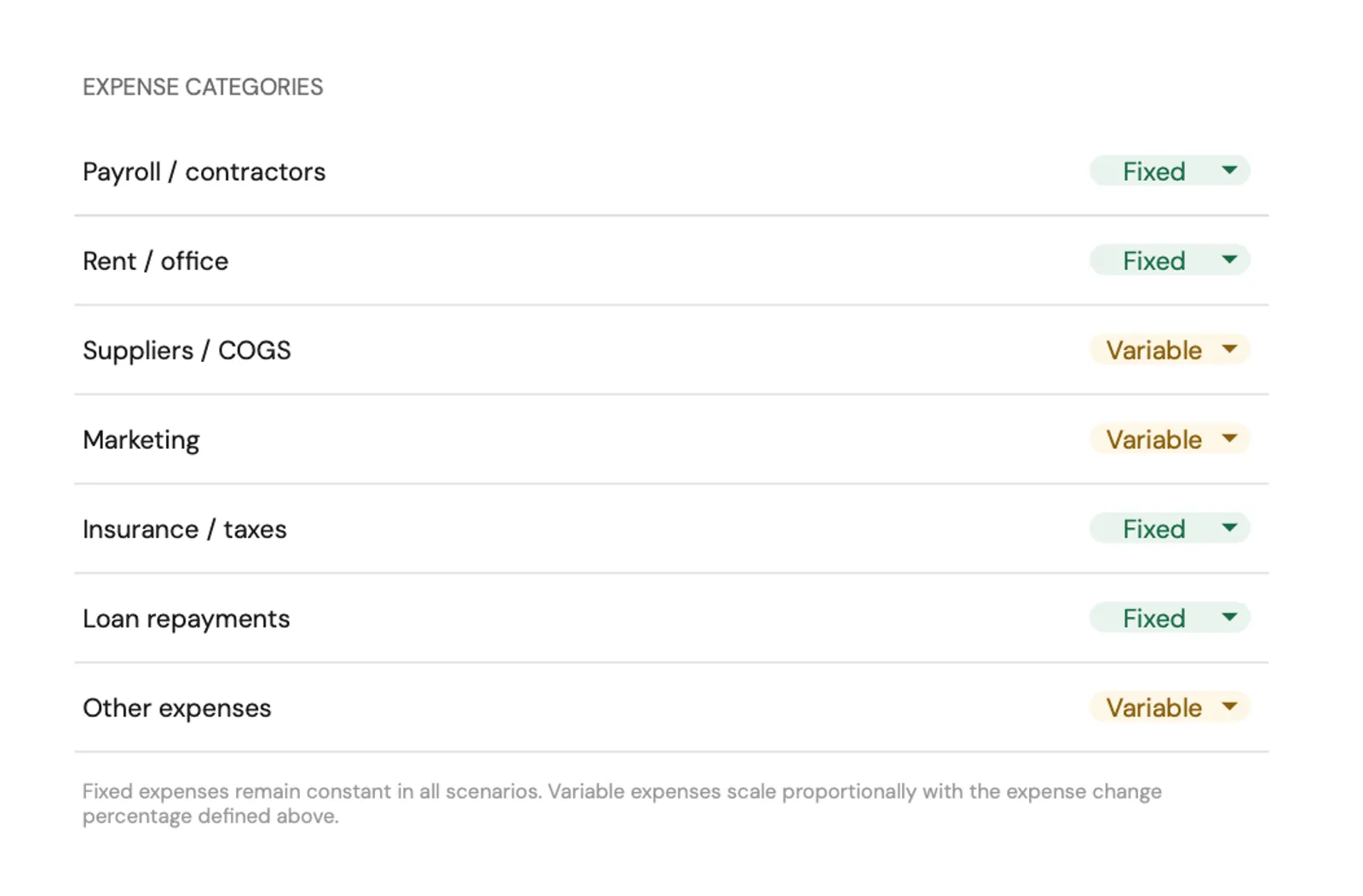

Set up expense categories for your business

Recommended Templates

The Right Templates for This Stage

Starting a business means managing two financial lives - personal and business. These templates cover both:

Forecast and track business cash flow month by month. See when you expect to break even, identify months where additional funding may be needed, and compare projections to actual results.

View templateTrack personal expenses separately to understand your exact monthly burn rate. Knowing your personal costs helps determine how much runway you have and when you need the business to start generating income.

View templateStay on top of quarterly estimated taxes and track deductible business expenses throughout the year. Particularly valuable in the first year when income is unpredictable and tax obligations are new.

View templateFree Tools

Calculators to Help You Plan

Common Questions

Starting a Business - Financial FAQ

How much money do I need to start a business?

It depends entirely on the business type. Service businesses (consulting, freelancing, coaching) can launch for $500-$5,000. Online businesses typically require $2,000-$20,000. Physical retail or restaurants may need $50,000-$200,000+. The key numbers to calculate: startup costs (one-time), monthly operating costs, and personal living expenses for the expected time to profitability.

How do I handle irregular income as a business owner?

One common approach: pay yourself a fixed "salary" from the business account to your personal account, based on the minimum you need for personal expenses. Let the business account absorb the fluctuations. When the business has surplus months, build a cash reserve. When income dips, the reserve covers the gap. A cash flow forecast helps anticipate lean months.

What business expenses are tax deductible?

Common deductions include: home office space (proportional to your home), internet and phone (business-use percentage), software and tools, marketing and advertising, professional services (accountant, lawyer), business insurance, travel for business purposes, vehicle use for business, and health insurance premiums for self-employed individuals. Track everything and consult a tax professional for your specific situation.

Can I use a spreadsheet to manage business cash flow?

Yes - and for early-stage businesses, a spreadsheet is often more practical than accounting software. The Business Cash Flow template tracks projected vs. actual income and expenses, shows your cash position month by month, and highlights when you might face shortfalls. Many founders use this alongside basic accounting software for the best of both.

Can't find the answer you're looking for? Contact our team

Ready to get started?

Download instantly and start managing your finances, or contact us to design a custom template package for your needs.