Cash Flow Forecast

Cash Flow Forecast Template for Nonprofits

Forecast grant funding, track donation cycles, manage program expenses, and plan around restricted fund requirements - all in a Google Sheets template built for cash flow management.

In Depth

Grants, Giving, and the Financial Pulse of Nonprofits

Nonprofit cash flow has a character distinct from any for-profit business because the relationship between spending and earning is fundamentally different. A business spends money to generate revenue. A nonprofit spends money to deliver its mission, and revenue comes from funders who believe in that mission enough to support it - often on their own timeline and with their own conditions. This means cash flow planning is less about optimizing a revenue engine and more about aligning multiple funding streams with ongoing program commitments.

The restricted versus unrestricted distinction is one that nonprofit leaders learn to watch closely. A bank balance of $300,000 might look healthy until you realize $250,000 is restricted to specific programs, leaving only $50,000 for general operations - payroll, rent, utilities, insurance. Some organizations with large bank balances still face genuine cash crunches because most of that cash cannot legally be spent on operating needs. Tracking unrestricted cash separately from total cash reveals the true operational picture.

Grant-funded organizations face a particular timing challenge when grants reimburse expenses rather than providing funds upfront. A government grant that requires spending first and submitting for reimbursement means the nonprofit needs working capital to bridge a 30 to 90 day gap between paying for program activities and receiving the grant payment. Across multiple reimbursement-based grants, this bridge financing need can reach into six figures - money the organization must have available even though it will eventually be repaid.

Individual donation patterns tend to cluster around year-end, with many nonprofits receiving 30-50% of individual contributions in November and December. This creates a Q4 cash surplus that must fund Q1 and Q2 operations when giving drops sharply. Organizations that have successfully built a monthly giving program often describe it as transformative for cash flow, even when the total annual amount from monthly donors is modest. The predictability of monthly gifts - $5,000 arriving reliably each month - can matter more to operational stability than a $60,000 annual total that arrives unevenly.

The Challenge

Cash Flow Challenges for Nonprofits

Nonprofits face unique cash flow challenges because revenue depends on external funding sources with their own timelines and restrictions. The gap between when grants are awarded, when funds are received, and when expenses are incurred creates persistent cash flow pressure.

Grant funding arrives on unpredictable schedules

A $100,000 grant might be awarded in March, with the first disbursement arriving in July. Government grants often reimburse expenses after they are incurred, creating a months-long cash gap. Foundation grants may disburse quarterly or annually. A nonprofit relying on 3-5 major grants faces the reality that each one has a different disbursement schedule, reporting timeline, and renewal uncertainty. If a grant is delayed by even one month, it can create a serious cash crunch.

Donation revenue is seasonal and unpredictable

Individual donations often cluster in Q4, with some organizations receiving 30-50% of annual individual giving in November and December. This creates a cash surplus in Q4 followed by a donation drought in Q1. Monthly donors provide more predictable cash flow, but typically represent a small percentage of total giving. Event-based fundraising adds another variable - a gala might generate $50,000 but requires $15,000-$25,000 in upfront costs months before the event.

Restricted funds cannot be used for general operations

Many grants and major donations carry restrictions - the money can only be spent on specific programs or purposes. A nonprofit might have $200,000 in the bank but only $30,000 available for general operations because the rest is restricted. Cash flow forecasting must separate restricted from unrestricted funds to show the true operating cash position. Spending restricted funds on non-approved purposes creates legal and compliance problems.

Program costs continue between funding cycles

Staff salaries, rent, and program operations do not pause when funding lapses between grant periods. A program funded by a grant that ends in June and resumes (hopefully) with a new grant in October faces four months of unfunded costs. The nonprofit must either maintain cash reserves, find bridge funding, or reduce program operations - each of which has consequences for mission delivery and staff retention.

Start forecasting your cash flow

Forecasting Guide

How to Forecast Cash Flow for Your Nonprofit

Nonprofit cash flow forecasting requires tracking multiple funding streams with different disbursement schedules and restrictions. Here is how to structure it using the Cash Flow Forecast template.

Revenue Categories

- Government grants (by grant)

- Foundation grants (by funder)

- Individual donations (monthly donors, one-time gifts)

- Corporate sponsorships

- Fundraising events (net of direct costs)

- Program service fees (earned revenue)

- Membership dues

Expense Categories

- Program staff salaries

- Administrative staff salaries

- Payroll taxes and benefits

- Rent and facilities

- Program supplies and materials

- Travel and transportation

- Insurance (D&O, general liability)

- Technology and software

- Fundraising costs

- Accounting and audit fees

- Professional development

- Utilities and communications

Cash Flow Timing

Map each grant's disbursement schedule onto the monthly forecast. Government reimbursement grants create the biggest timing challenge - you spend the money first and wait 30-90 days for reimbursement. For donation revenue, use historical patterns to project monthly giving (heavily weighted to Q4). Keep unrestricted and restricted cash positions separate in your forecast to show the true operating picture.

See It In Action

What the template looks like

Browse through the template to see dashboards, forecasting, actuals tracking, and scenario planning.

- Visual cash flow dashboard

- Forecast vs actuals comparison

- Scenario planning tools

- Customizable categories

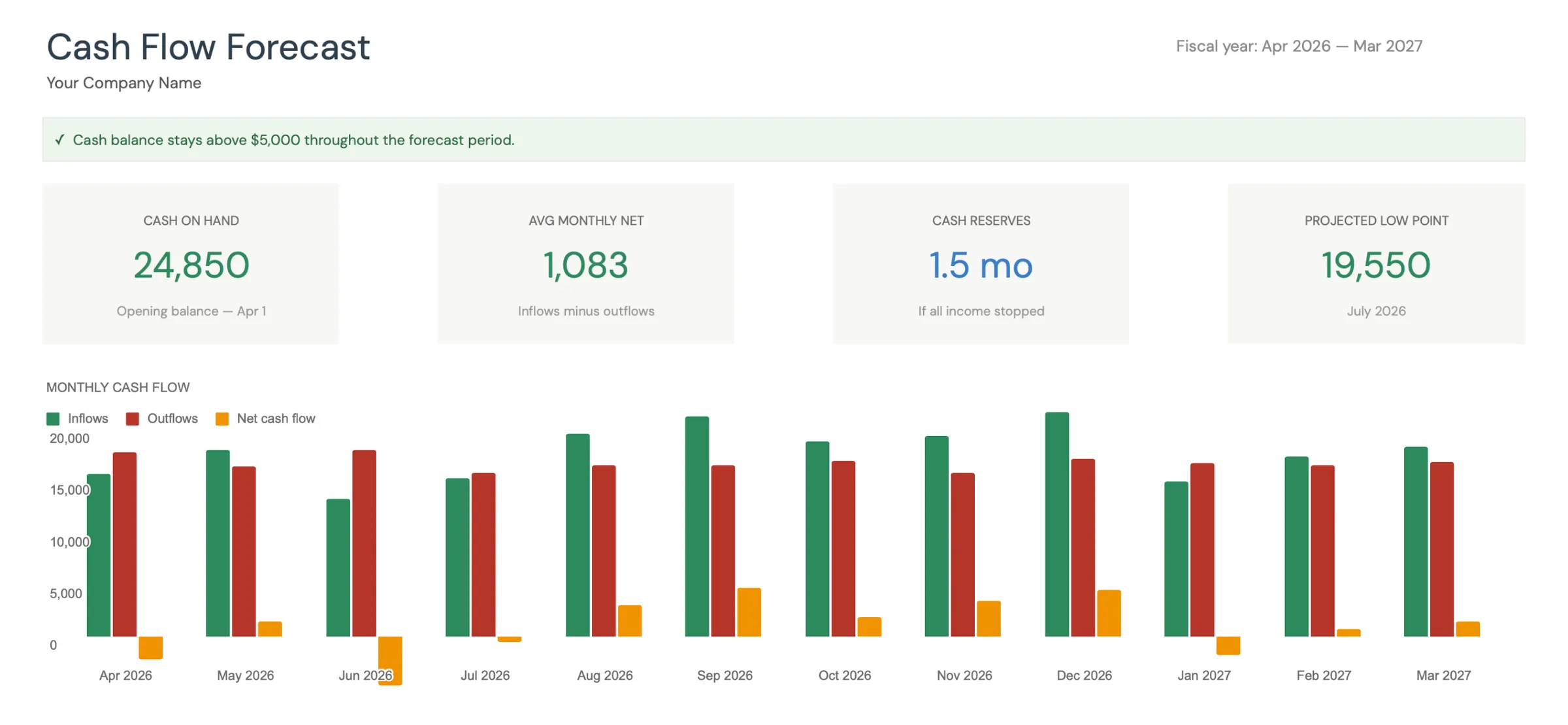

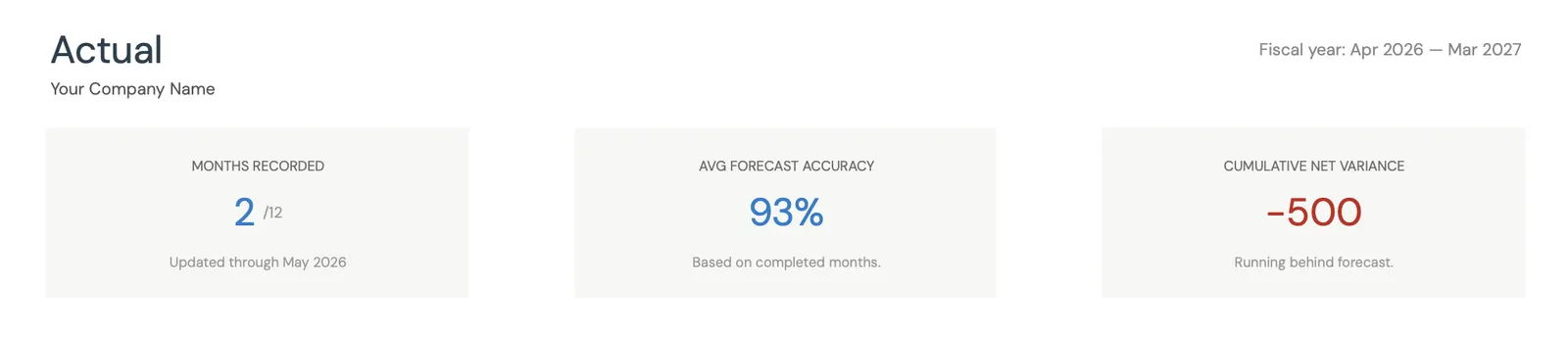

Monthly cash flow overview with KPIs and charts

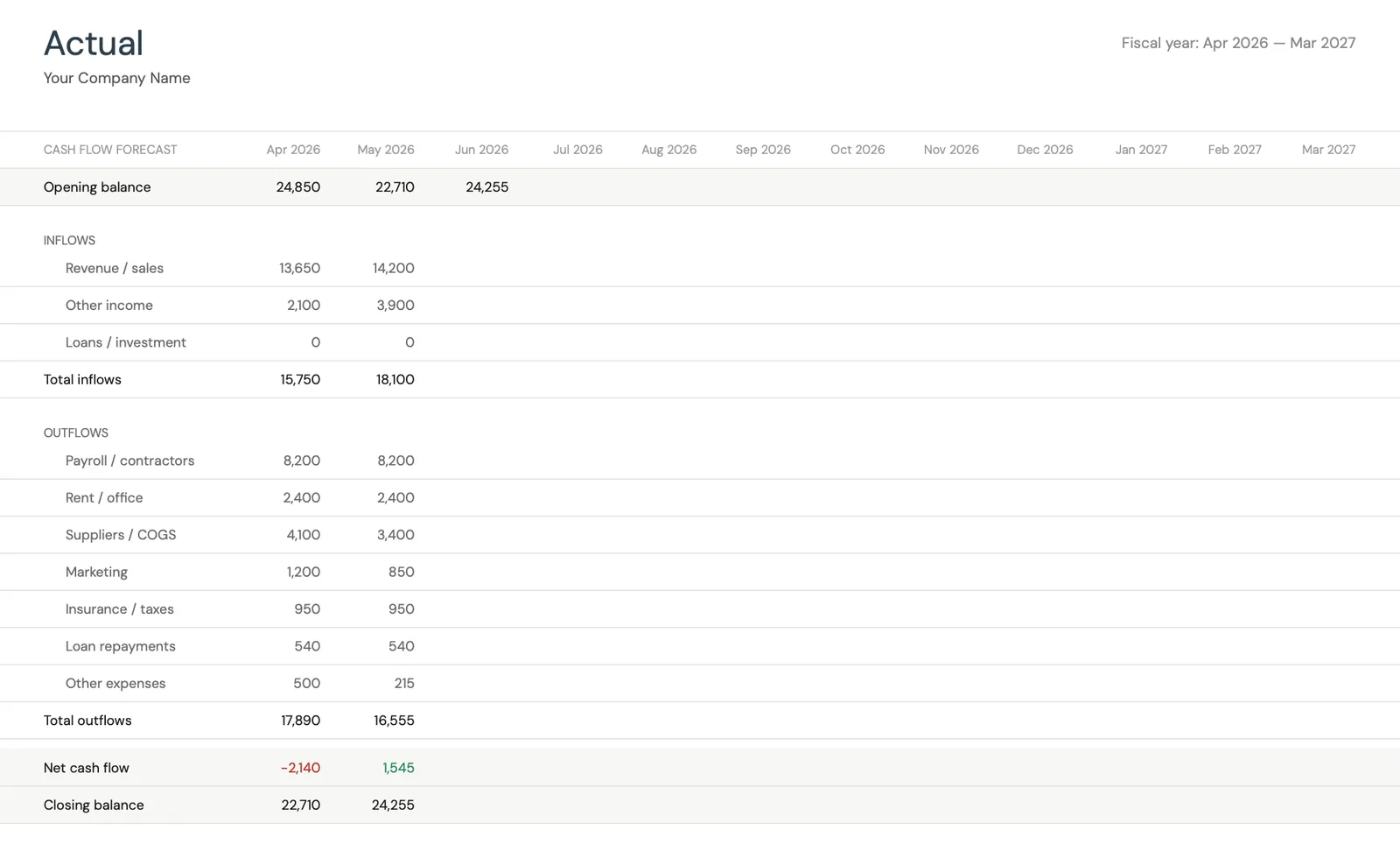

Track actual cash flow against your forecast

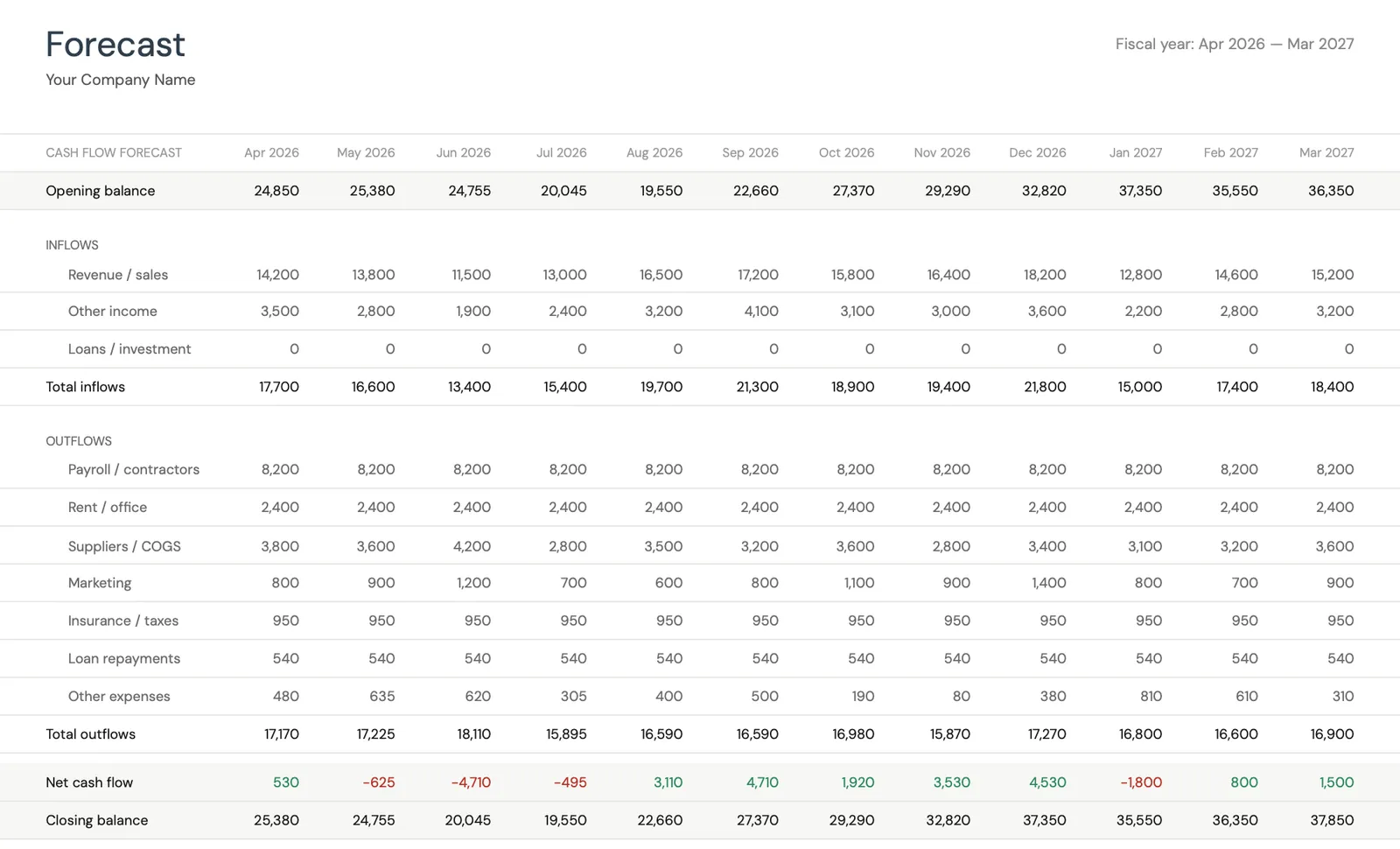

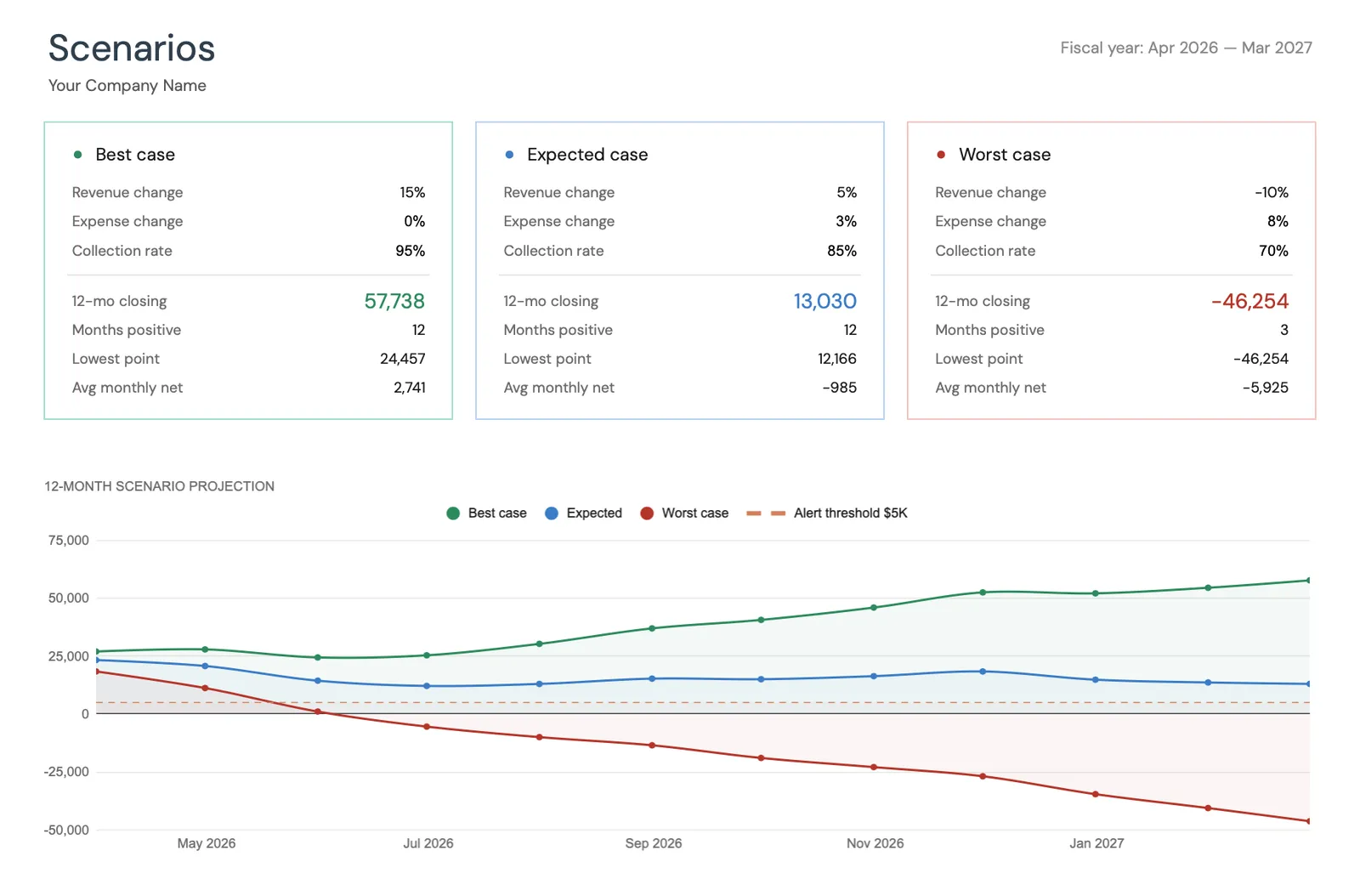

Project cash flow 12 months ahead

Key performance indicators for your cash flow

Model different scenarios for your business

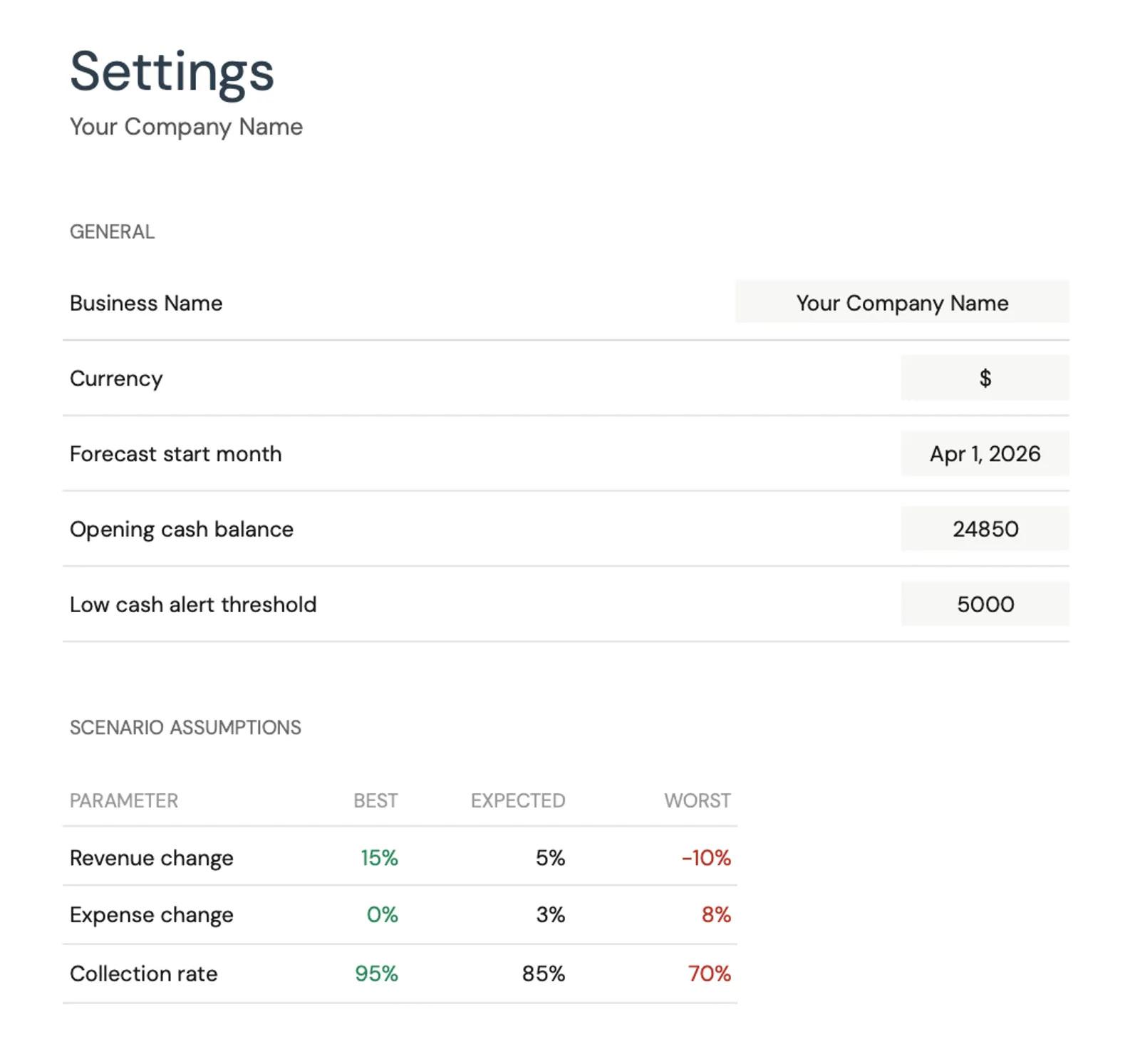

Customize categories for your business type

What You Get

How This Template Supports Nonprofit Cash Flow

Multi-source funding tracking

Track each funding source separately with its own disbursement schedule and restrictions. See how grants, donations, and earned revenue combine to create your total cash position, and identify months where specific funding sources create gaps.

Restricted vs unrestricted cash visibility

Separate restricted funds from general operating cash to see your true available cash position. Having $200,000 in the bank means little if $170,000 is restricted to specific programs.

Grant disbursements vs your timeline

Compare projected funding disbursements against actuals. Grant disbursement delays are common - tracking the variance helps build realistic timing assumptions and identifies when cash reserves will be tested.

12-month funding cycle cash outlook

See your projected cash position across the full funding cycle. Identify months where grant gaps create cash deficits, plan fundraising events and campaigns around projected low points, and determine your operating reserve needs.

Common Questions

Cash Flow for Nonprofits - FAQ

How much operating reserve should a nonprofit maintain?

A commonly referenced guideline is 3-6 months of operating expenses in unrestricted reserves. For a nonprofit with $50,000/month in expenses, that means $150,000-$300,000. Many nonprofits fall short of this target. The cash flow forecast helps determine the minimum reserve needed by identifying the largest projected cash gap in the 12-month outlook.

How do I handle grants that reimburse expenses after the fact?

Reimbursement-based grants require working capital to fund expenses before the grant payment arrives. Enter the expense when it occurs and the reimbursement when you expect to receive it (typically 30-90 days later). The gap between the two shows the working capital needed. If you are spending $10,000/month on a reimbursable grant with 60-day reimbursement, you need $20,000 in working capital for that grant alone.

How do I forecast individual donations?

Use historical giving data as the baseline. Most nonprofits see consistent monthly giving patterns once they have 2-3 years of data. Apply a seasonal adjustment (heavier in Q4) and a growth or decline factor based on donor retention and acquisition trends. Be conservative - donor giving is one of the less predictable revenue sources.

What if a major grant is not renewed?

Model this scenario in your forecast. If a $150,000 grant (25% of your budget) is up for renewal, create a version of the forecast that assumes it is not renewed. This immediately shows the cash flow impact and the timeline for finding replacement funding. Having this scenario modeled before the decision comes allows the board and leadership to plan proactively.

Can this template handle multiple program budgets?

The template tracks overall organizational cash flow. For program-level budgeting, you can create category lines for each program's revenue and expenses. The consolidated view shows total cash position while the line items reveal which programs are self-sustaining and which require general operating support.

Can't find the answer you're looking for? Contact our team

Forecast cash flow for your nonprofit

One-time purchase. No subscription. Your financial data stays in your Google Drive.