Life Event Guide

Financial Planning When Managing Rental Properties

Rental properties generate income but also create complex cash flow, tax, and maintenance tracking needs. Staying on top of the numbers is what separates profitable landlording from expensive headaches.

Financial Impact

The Financial Impact of Rental Property Management

Rental properties are businesses, even if you only own one unit. The financial complexity increases with each property, and the difference between perceived returns and actual returns often surprises landlords who are not tracking carefully.

Cash flow is rarely as simple as rent minus mortgage

A property renting for $2,000/month with a $1,400 mortgage appears to generate $600/month cash flow. But add property taxes ($250/month), insurance ($100/month), maintenance reserves ($200/month at 10% of rent), vacancy allowance ($167/month at one month per year), property management fees if applicable ($200/month at 10%), and capital expenditure reserves ($100/month). Realistic cash flow on that same property might be negative $417/month before any unexpected expenses.

Tax deductions can significantly improve the real return

Rental property offers substantial tax benefits: mortgage interest deduction, depreciation (the cost of the building spread over 27.5 years), property tax deduction, maintenance and repair costs, insurance, travel expenses for property management, and professional fees. Depreciation alone on a $300,000 property (excluding land value of approximately $75,000) provides roughly $8,182/year in deductions - reducing taxable rental income even when you have positive cash flow.

Vacancy and turnover costs are commonly underestimated

The average rental vacancy rate in the US is 5-8%, but turnover costs extend beyond lost rent. Between tenants: cleaning ($200-$500), repairs and paint ($500-$2,000), advertising ($100-$300), and time spent showing the unit and screening applicants. A single turnover can cost $2,000-$5,000 plus the lost rent. Properties with lower tenant turnover are often more profitable even at slightly below-market rents.

Capital expenditures create lumpy, large expenses

Roofs ($8,000-$15,000), HVAC systems ($5,000-$12,000), water heaters ($1,500-$3,000), appliance replacements ($2,000-$5,000), and flooring ($3,000-$8,000) all have finite lifespans. A property that generates positive cash flow for three years can appear to lose money when a major system needs replacement. Maintaining a capital expenditure reserve of 5-10% of rental income smooths these costs over time.

Getting Ready

How to Track Rental Property Finances

Track income and expenses per property separately

Even if you own multiple properties, keep the financials separate. Each property has its own income, expenses, mortgage, and performance. Combining them hides underperformers and makes tax preparation harder. Record rent received, late fees, pet fees, and any other income separately from each expense category. This per-property clarity is essential for knowing which properties are actually earning their keep.

Maintain monthly cash flow tracking

Record all income and expenses monthly for each property. Categories typically include: rent received, mortgage payment (split into principal and interest for tax purposes), property taxes, insurance, repairs and maintenance, utilities (if landlord-paid), property management fees, and HOA fees. The monthly cadence catches problems early - a property that is consistently cash-flow negative may need a rent adjustment or cost reduction.

Set up reserves for vacancies and capital expenditures

Transfer a percentage of each rent payment into separate reserve accounts. A common approach: 5% for vacancy reserves and 5-10% for capital expenditure reserves. On $2,000/month rent, that is $200-$300/month set aside. When a vacancy or major repair occurs, the funds are already available rather than creating a financial emergency. Track these reserves as part of your rental property accounting.

Track all tax-deductible expenses throughout the year

Waiting until tax season to reconstruct expenses means missing deductions. Track every deductible expense as it occurs: mileage to and from properties, materials and supplies, contractor payments, insurance premiums, property tax payments, mortgage interest, and professional fees (accountant, attorney, property manager). A running log with dates, amounts, and categories makes tax preparation straightforward.

Calculate actual return on investment annually

Once a year, calculate the true return: total cash flow (rent minus all expenses), plus equity buildup (principal paid on mortgage), plus tax benefits (deductions times your marginal tax rate), plus or minus property value change. Compare this total return to what the same capital would earn invested elsewhere. This honest assessment reveals whether each property is genuinely a good investment or just feels like one.

See The Templates

Tools for this stage of life

Browse the templates that help with financial planning during major life transitions.

- Financial planning dashboard

- Monthly budget tracking

- Net worth over time

- Goal setting and tracking

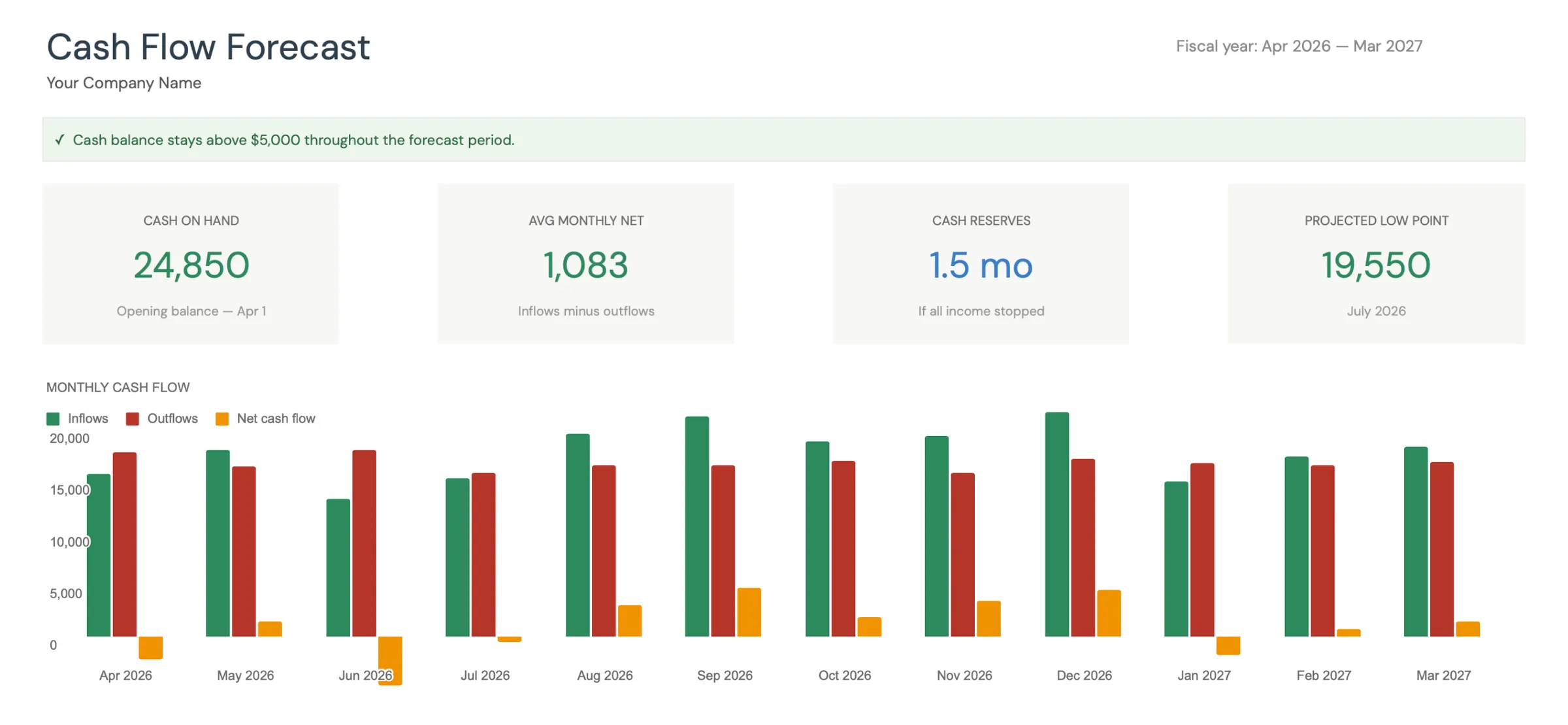

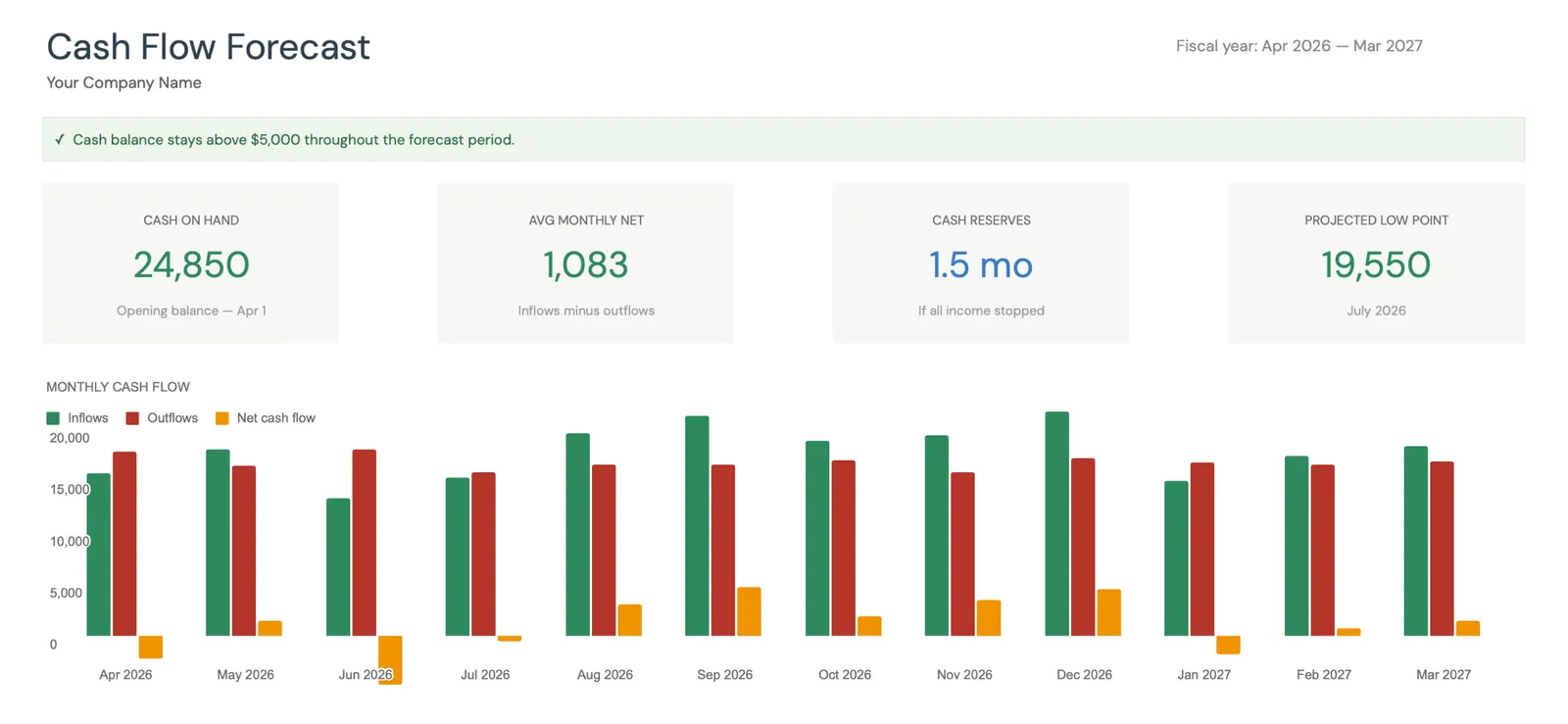

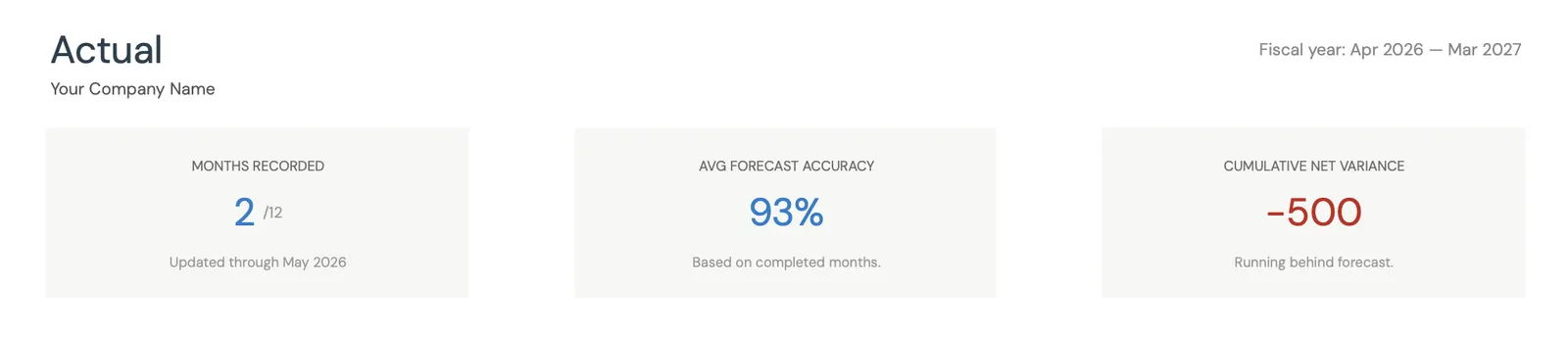

Visual dashboard with cash flow projections and trends

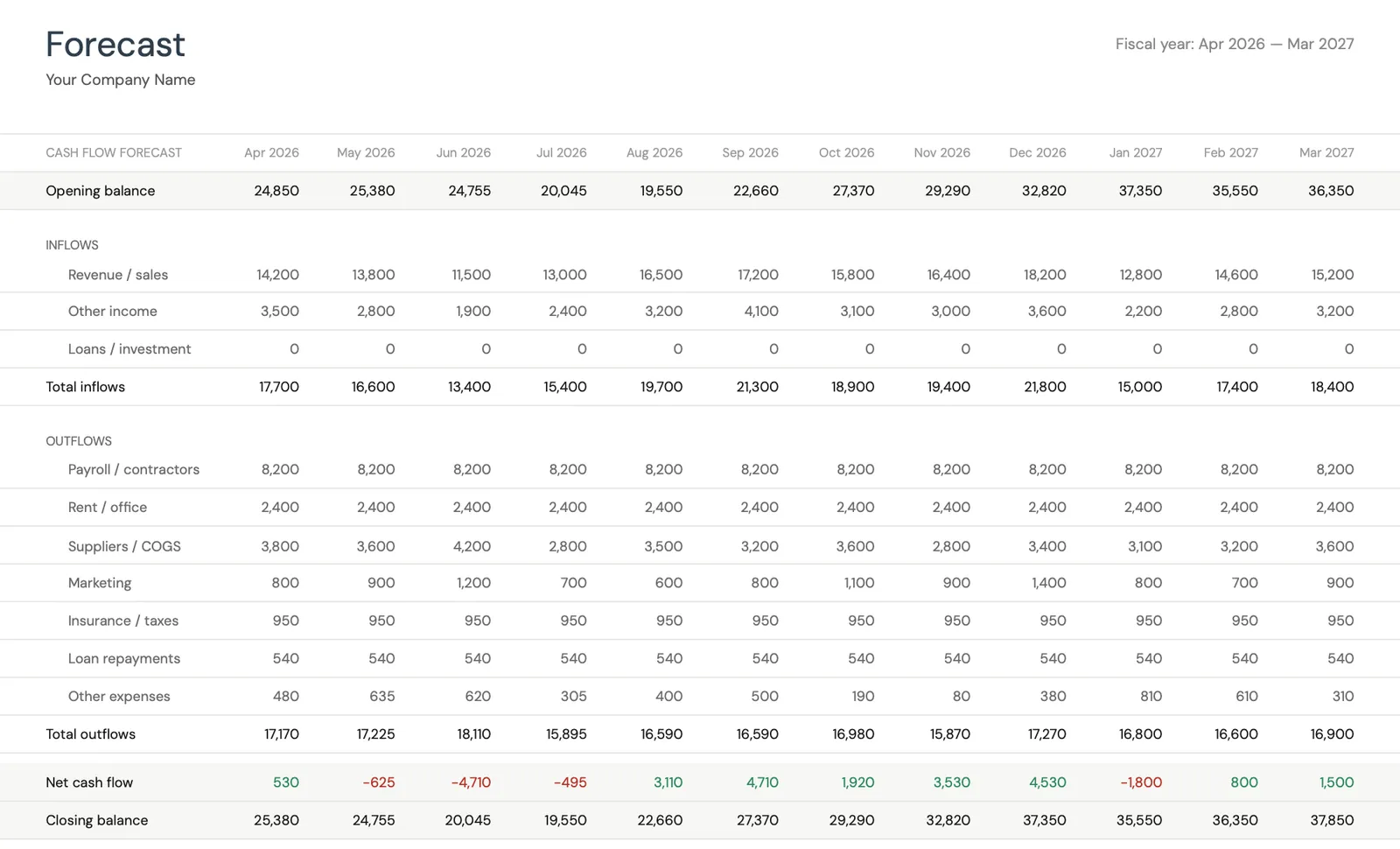

Monthly cash flow forecast with income and expenses

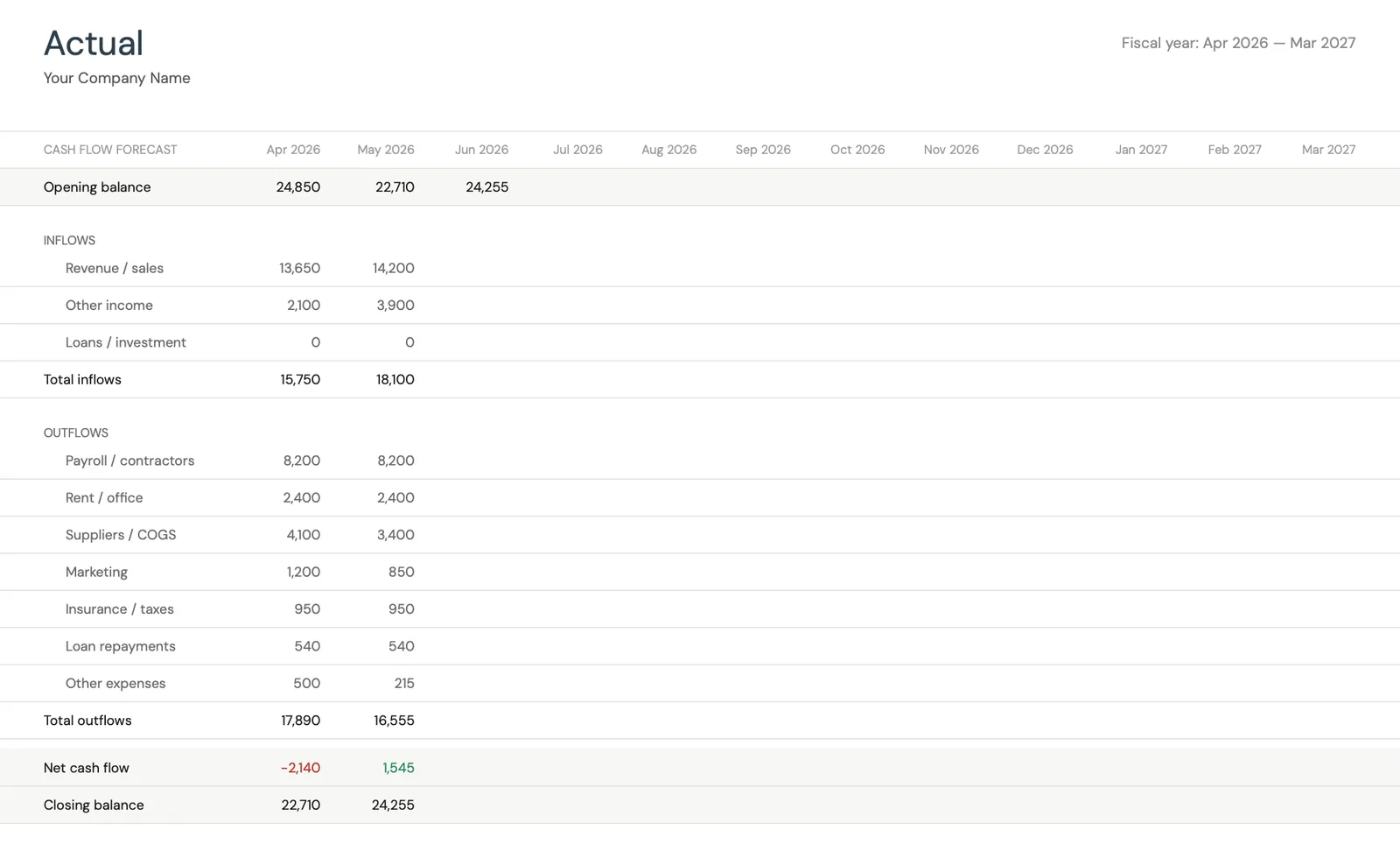

Track actual cash flow against your forecast

Key performance indicators for your cash flow

Monitor closing balances over time

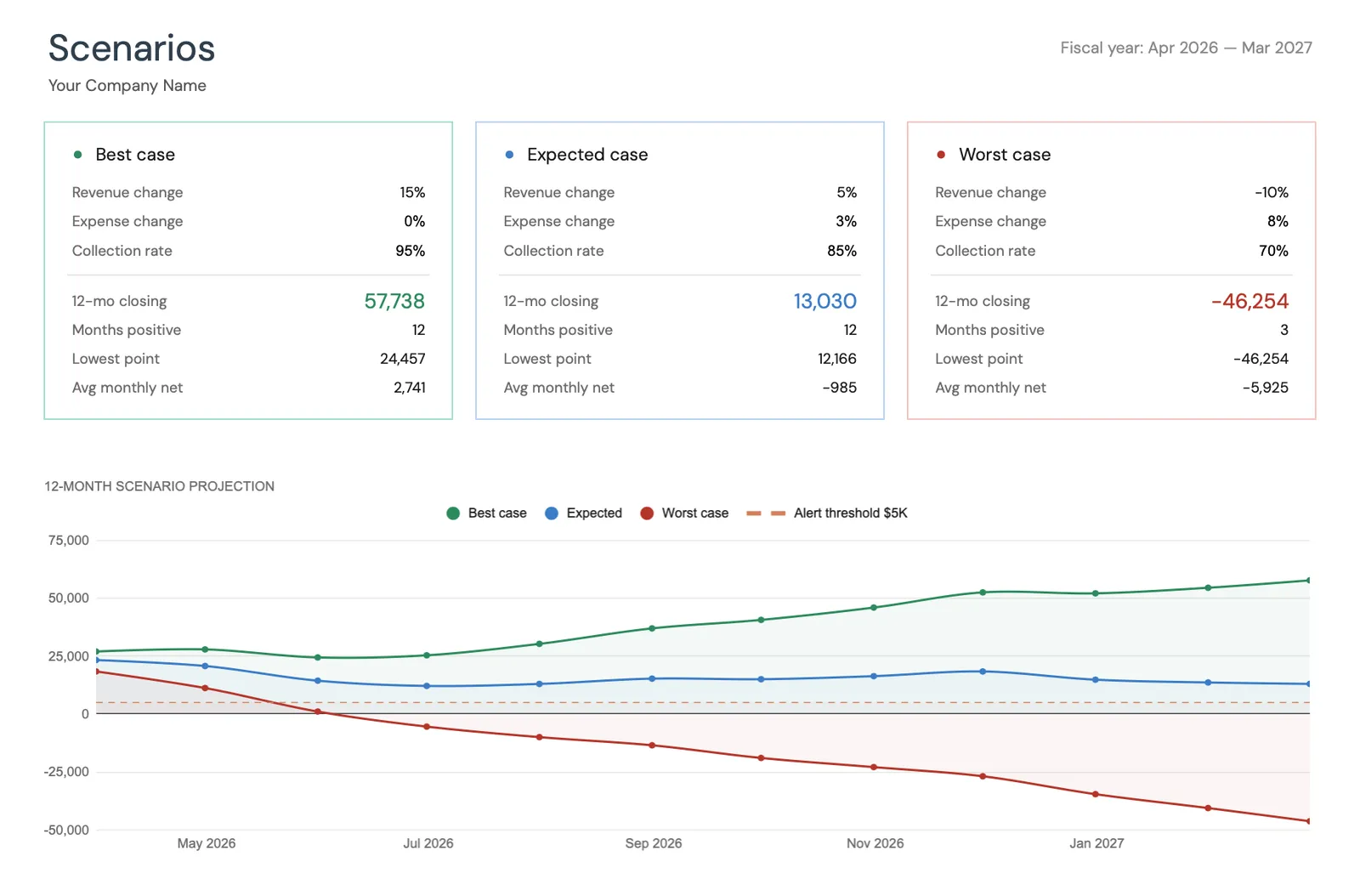

Model different business scenarios and their impact

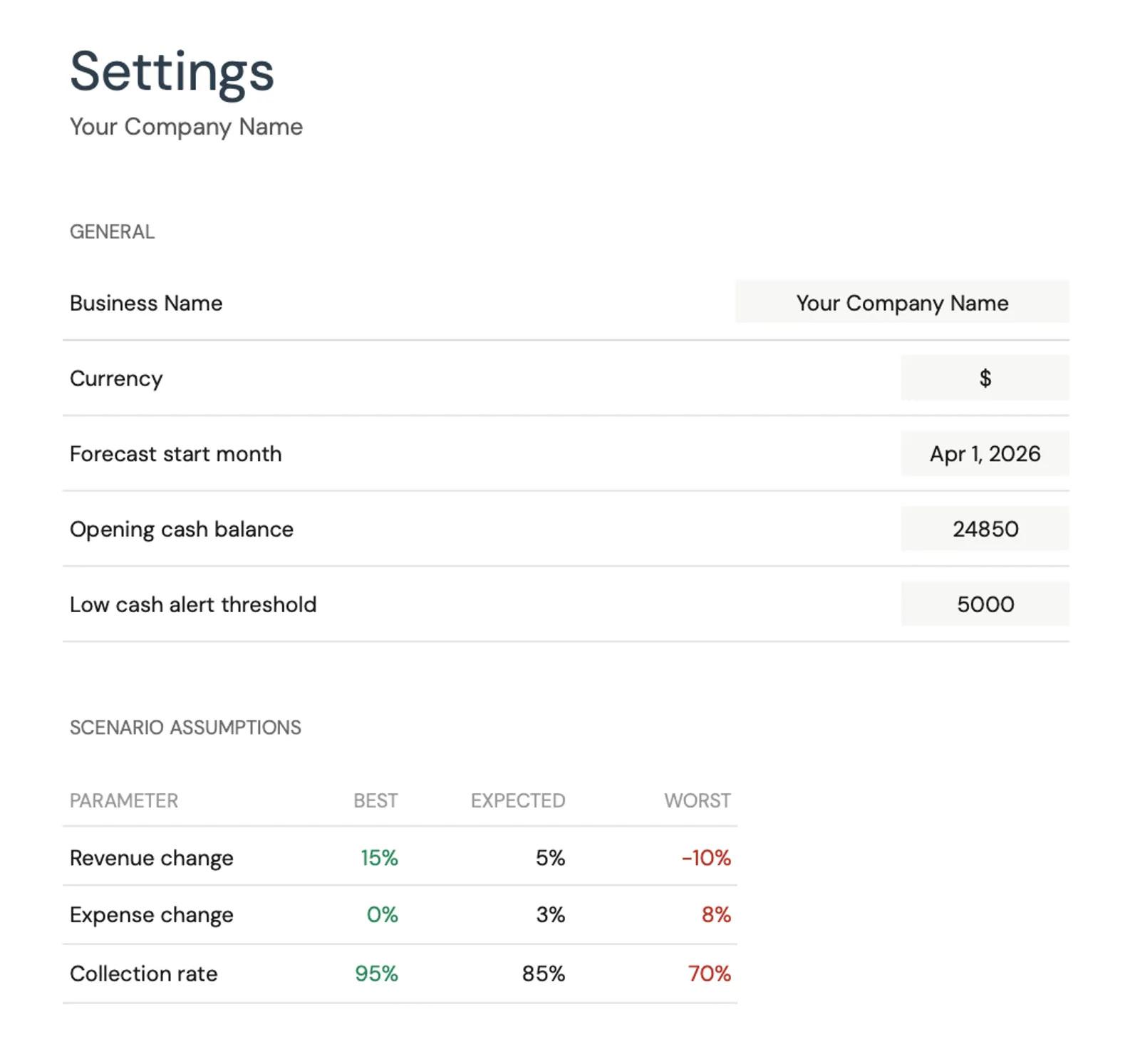

Configure income categories and settings

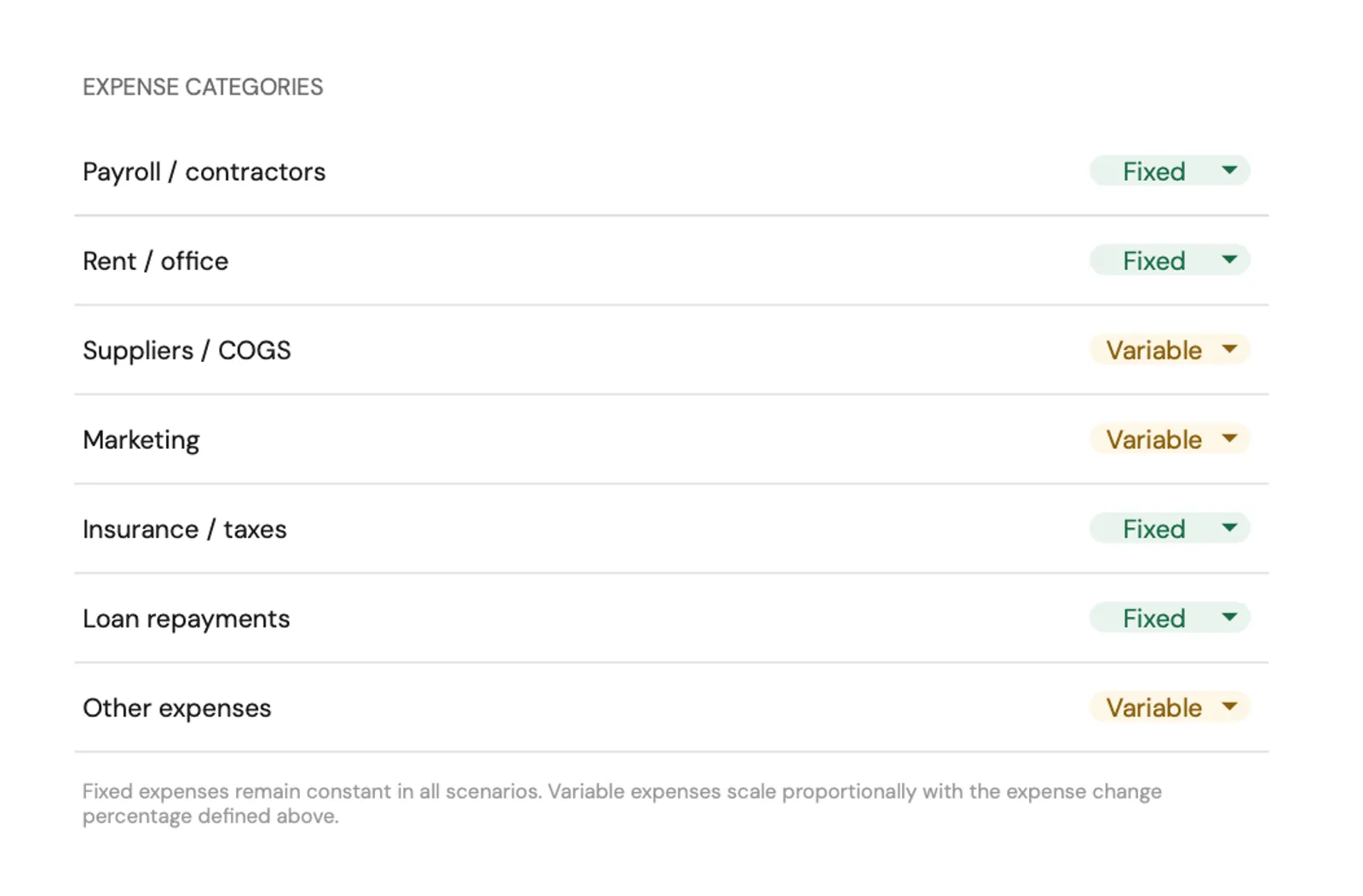

Set up expense categories for your business

Recommended Templates

The Right Templates for This Stage

Rental property management requires ongoing cash flow tracking, asset monitoring, and tax preparation. These templates handle the key areas:

Track rental income and expenses per property on a monthly basis. See cash flow trends, identify seasonal patterns, and forecast future income. Treats each property like the small business it is.

View templateMonitor total portfolio value including property equity, mortgage balances, and reserve accounts. Seeing how rental properties fit into your overall financial picture helps with decisions about acquiring, holding, or selling properties.

View templateOrganize all rental property tax deductions throughout the year - depreciation, mortgage interest, repairs, insurance, property taxes, and professional fees. Reduces tax-season stress and helps ensure no deductions are missed.

View templateFree Tools

Calculators to Help You Plan

Common Questions

Managing Rental Properties - Financial FAQ

How do I track rental property income and expenses?

Keep a separate accounting for each property with monthly entries for all income (rent, fees) and expenses (mortgage, taxes, insurance, repairs, management fees). Use a cash flow spreadsheet that shows net income per property per month. This per-property, per-month tracking reveals patterns and problems that annual summaries miss.

What percentage of rent should I set aside for reserves?

A common guideline is 5% for vacancy and 5-10% for capital expenditures and maintenance. On $2,000/month rent, that means setting aside $200-$300/month. Older properties or those with aging systems (15+ year old roof, older HVAC) may warrant higher reserves. Properties with newer systems and long-term tenants can sometimes operate with lower reserves.

What rental property expenses are tax deductible?

Most expenses related to rental property ownership and management are deductible: mortgage interest, property taxes, insurance, repairs and maintenance, depreciation, property management fees, advertising for tenants, legal and accounting fees, travel to and from the property, and home office expenses if you manage properties from home. Keep receipts and records for all expenses.

How do I know if my rental property is actually profitable?

True profitability includes four components: cash flow (rent minus all expenses including reserves), equity buildup (mortgage principal reduction), tax benefits (deductions reducing your tax bill), and appreciation (property value changes). A property with negative monthly cash flow can still be profitable when equity buildup and tax benefits are included. Calculate all four components annually for an honest assessment.

How many properties can I manage with a spreadsheet?

Spreadsheets work well for 1-10 properties. Beyond that, dedicated property management software may be more efficient. The key is consistency - updating income and expenses monthly and maintaining reserve tracking. A well-organized spreadsheet with separate tabs per property and a summary dashboard provides excellent visibility for most individual landlords.

Can't find the answer you're looking for? Contact our team

Ready to get started?

Download instantly and start managing your finances, or contact us to design a custom template package for your needs.