Budget Guide

How to Budget for a Small Business

About 82% of small businesses that fail cite cash flow problems as a factor. A business budget that forecasts revenue, tracks expenses by category, and projects cash flow 3-12 months ahead turns financial guesswork into a manageable monthly process.

In Depth

Cash Flow Is the Heartbeat of Small Business

The statistic that 82% of failed businesses cite cash flow problems is not about profitability - it is about timing. A business can be profitable on paper while simultaneously running out of cash to pay next week's expenses. Revenue arrives on one schedule (often delayed by 30, 60, or 90 days in B2B contexts), while expenses demand payment on another. The gap between when money is earned and when it is collected is where cash flow problems live, and a forecast that maps both timelines is the primary tool for managing that gap.

Tax obligations create a particularly dangerous cash flow trap for new business owners. Unlike employment income where taxes are withheld automatically, business income arrives in full - and the tax bill comes later. Business owners who spend revenue without setting aside 25-35% for taxes face an annual or quarterly reckoning that can threaten the business itself. A separate tax savings account, funded as revenue arrives, transforms this from a crisis point into a routine part of financial operations.

The boundary between personal and business finances is one of the most important distinctions a small business owner can maintain. Commingled finances make it nearly impossible to determine true business profitability, complicate tax preparation, and can create legal liability issues for LLCs and corporations. A dedicated business bank account - paired with a cash flow template that tracks business finances separately - establishes the clarity needed to make informed decisions about both the business and personal financial health.

Cost Breakdown

Common Small Business Cost Categories

Business costs vary dramatically by industry and business model. These categories cover the most common expense areas that small business owners need to budget for.

Rent & Facilities

5-15% of revenueOffice, retail, or warehouse space - some businesses operate remotely

Payroll & Benefits

25-50% of revenueOften the largest ongoing expense for service-based businesses

Marketing & Advertising

5-15% of revenueDigital marketing, advertising, content creation, and sales tools

Software & Technology

3-8% of revenueAccounting, CRM, communication, and industry-specific tools

Insurance

2-5% of revenueLiability, property, workers comp, and professional insurance

Taxes & Professional Services

10-30% of profitIncome tax, self-employment tax, accountant, and legal fees

Budgeting Steps

Steps to Budget for a Small Business

Separate personal and business finances

A dedicated business bank account and credit card make expense tracking straightforward and are essential for accurate tax reporting. Mixing personal and business finances creates accounting headaches that get worse over time.

Forecast cash flow, not just profit

A business can be profitable on paper but run out of cash if payment timing is off. Cash flow forecasting tracks when money actually arrives and leaves - not just when it is earned or owed. This prevents the common problem of growing businesses running short on cash.

Plan for taxes quarterly

Self-employed individuals and small business owners typically owe quarterly estimated tax payments. Setting aside 25-35% of profit for taxes as it is earned prevents the painful annual tax bill. A separate tax savings account keeps these funds from being spent.

Build a business emergency fund

Just like personal finances, businesses benefit from cash reserves. Having 3-6 months of operating expenses saved helps weather slow periods, unexpected costs, and seasonal fluctuations without taking on debt or cutting essential expenses.

Review the budget monthly against actuals

Comparing budgeted numbers to actual results each month reveals trends before they become problems. Revenue shortfalls, expense creep, and seasonal patterns become visible through regular review. This habit is one of the most valuable things a business owner can do.

See The Template

Tools for small business budgeting

Browse the template features that help with small business financial planning.

- Automatic calculations

- Visual charts and summaries

- Customizable categories

- Works in Google Sheets and Excel

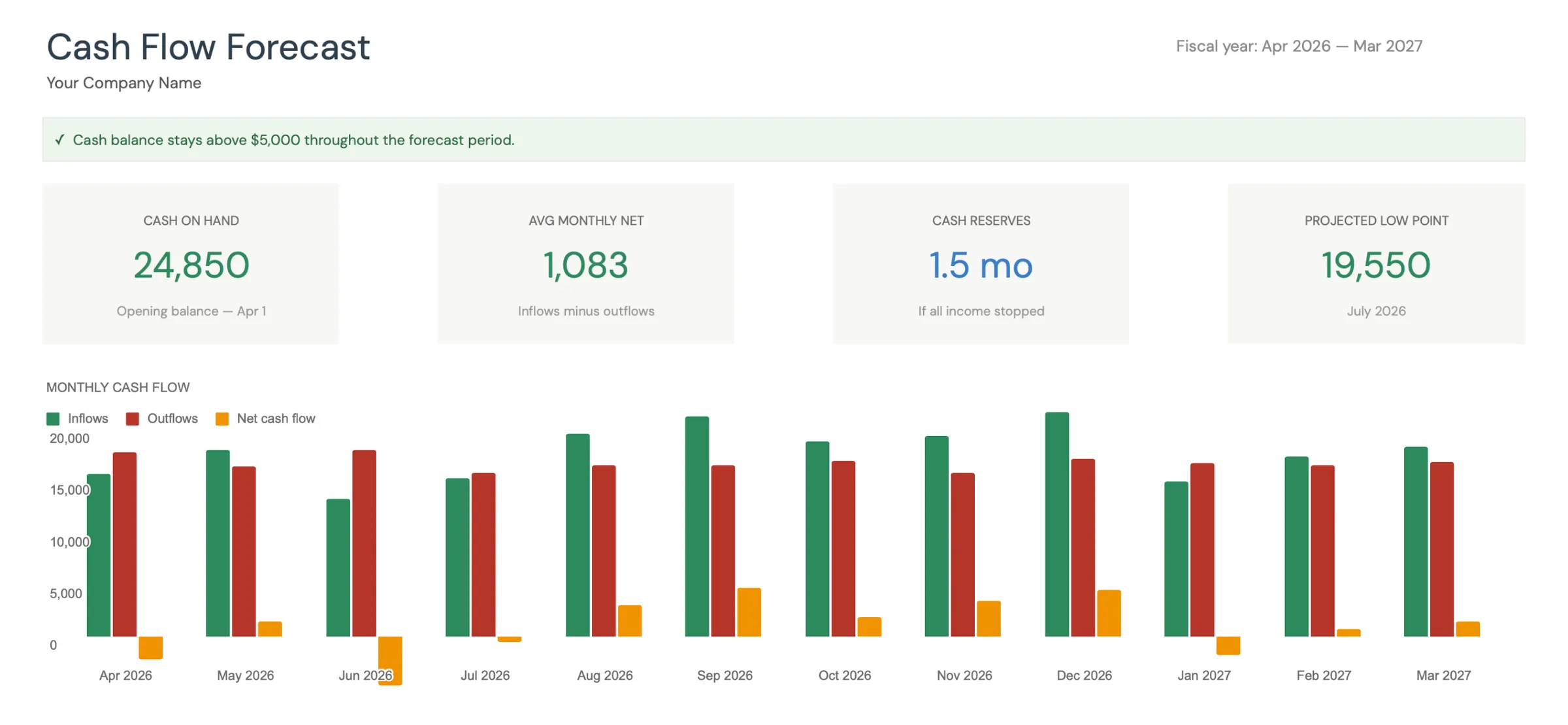

Visual dashboard with cash flow projections and trends

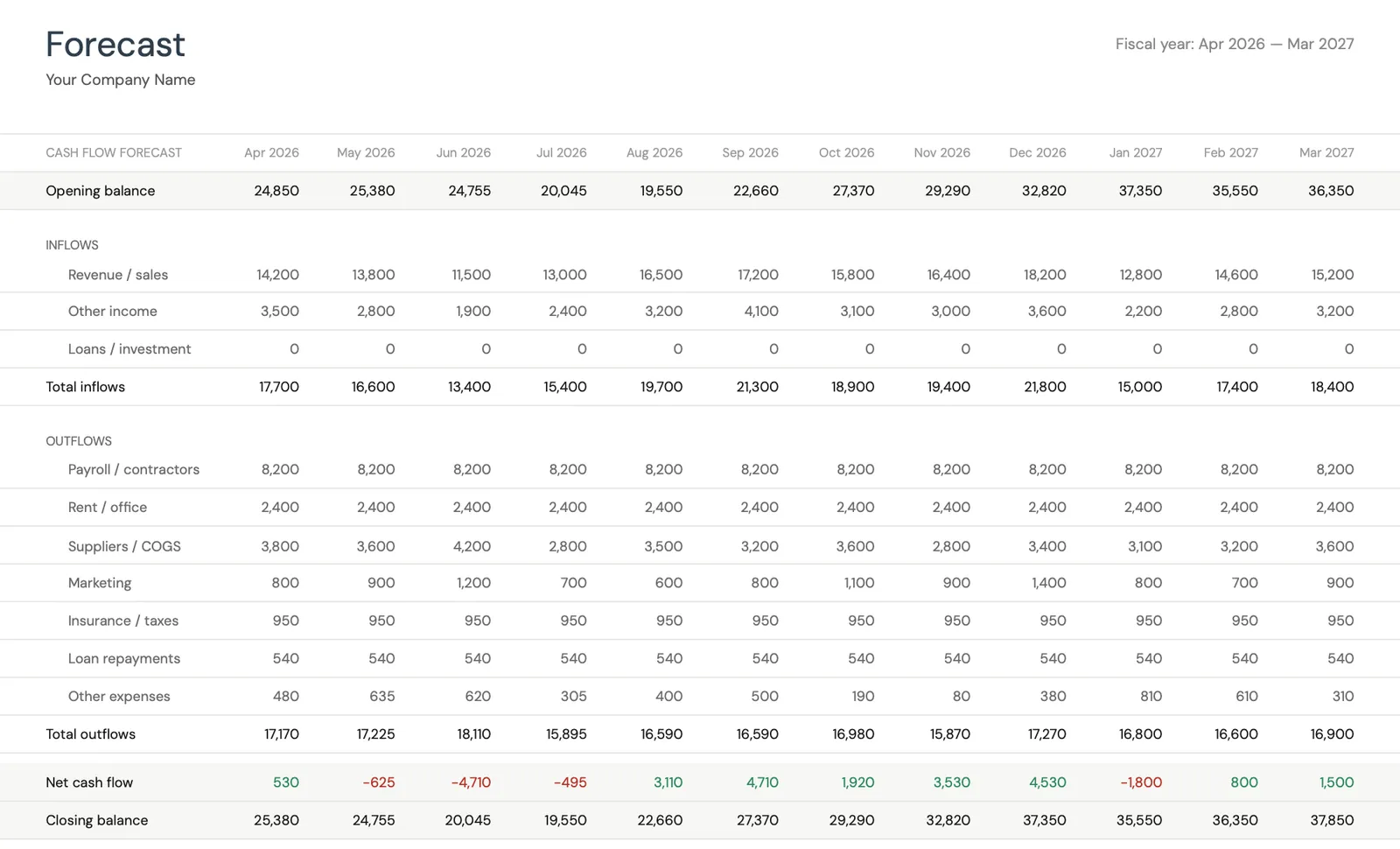

Monthly cash flow forecast with income and expenses

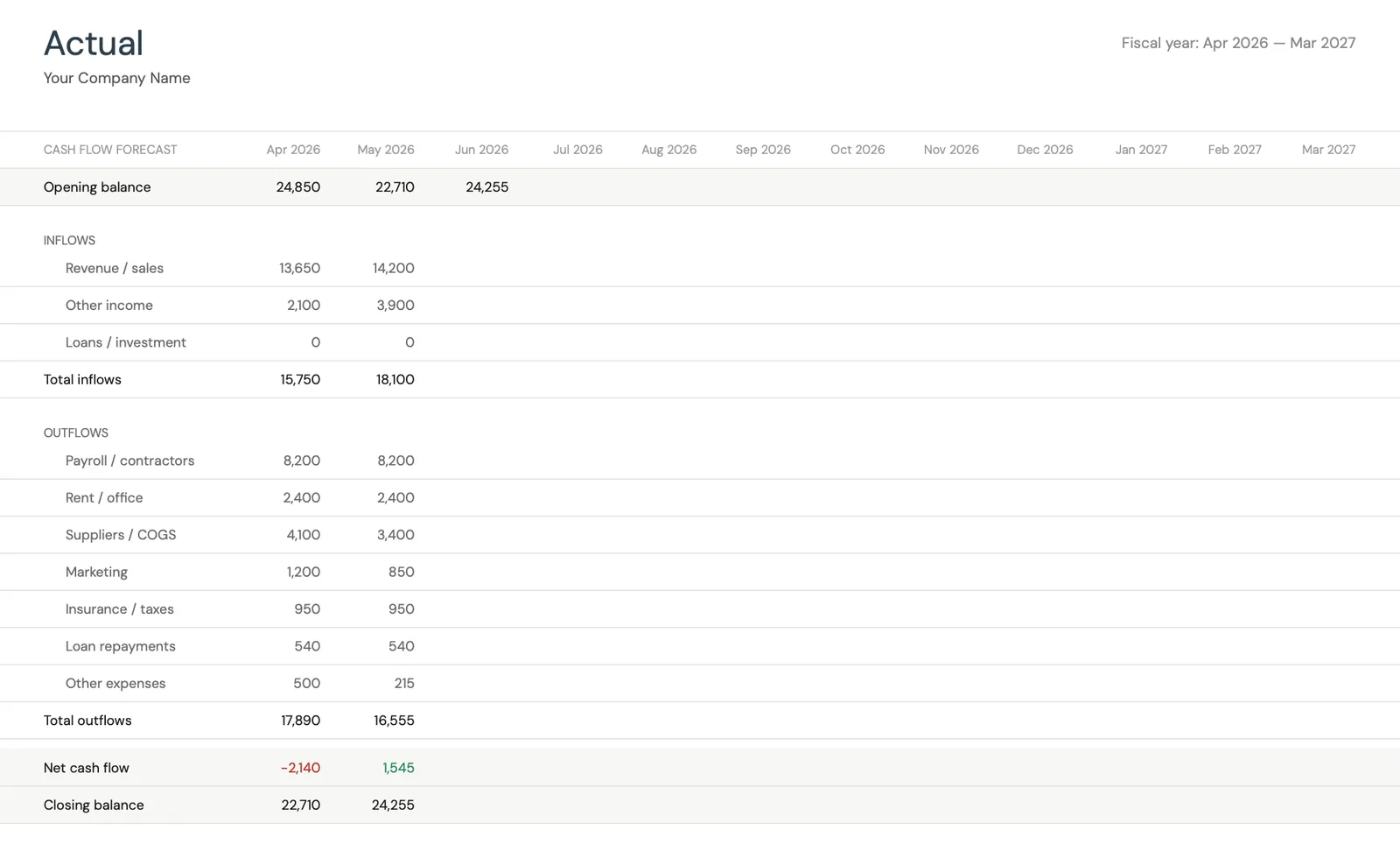

Track actual cash flow against your forecast

Key performance indicators for your cash flow

Monitor closing balances over time

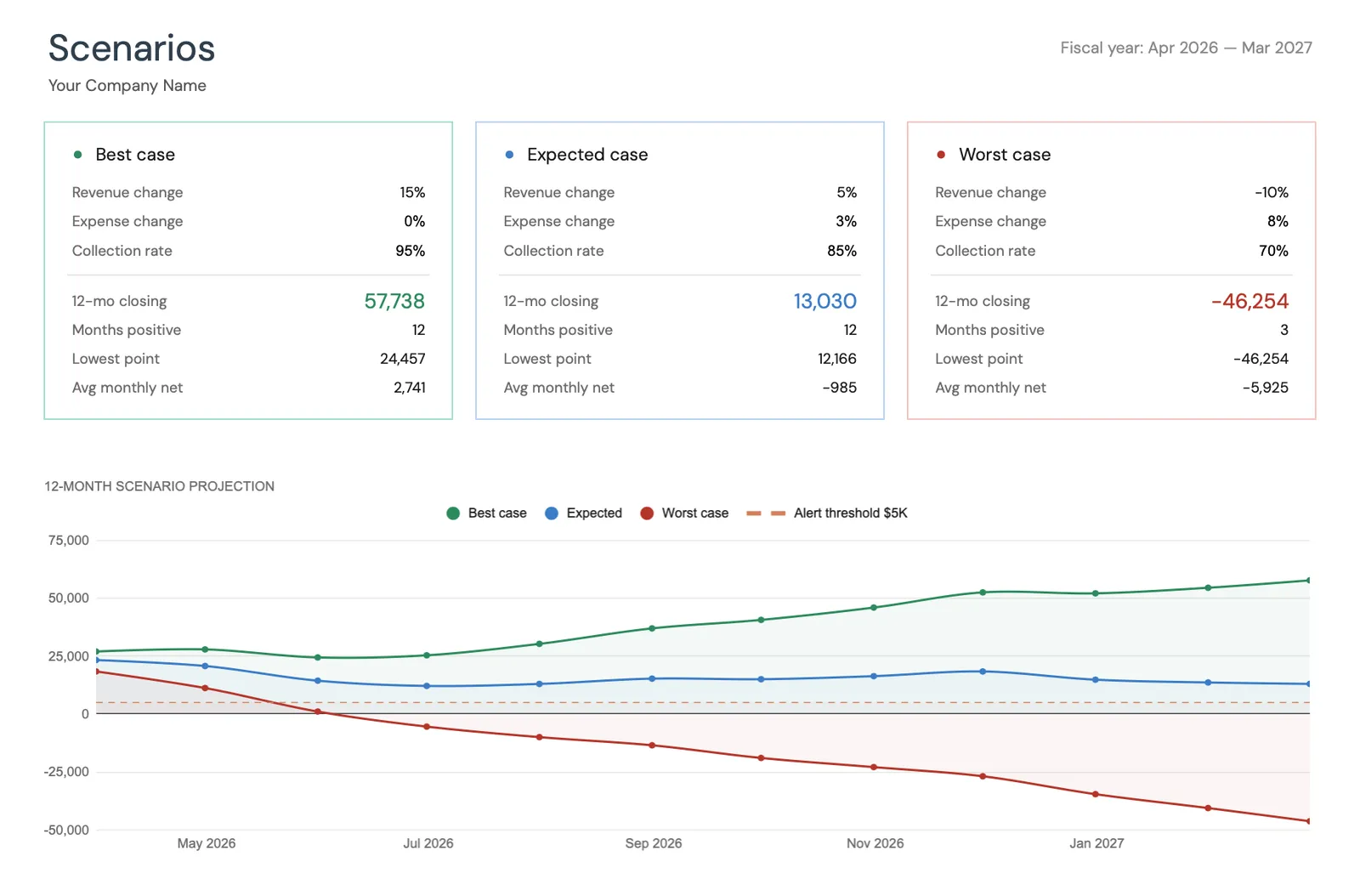

Model different business scenarios and their impact

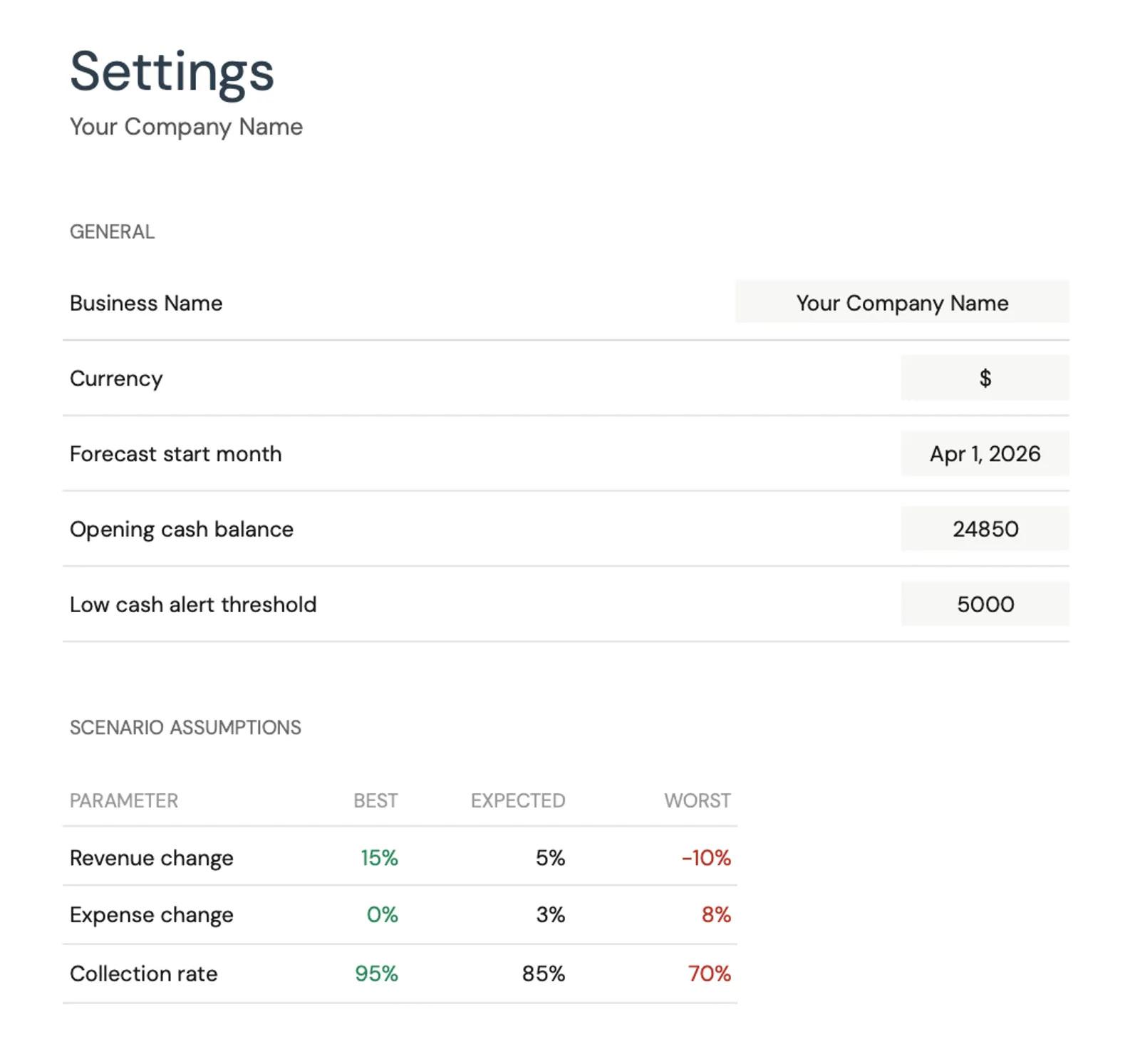

Configure income categories and settings

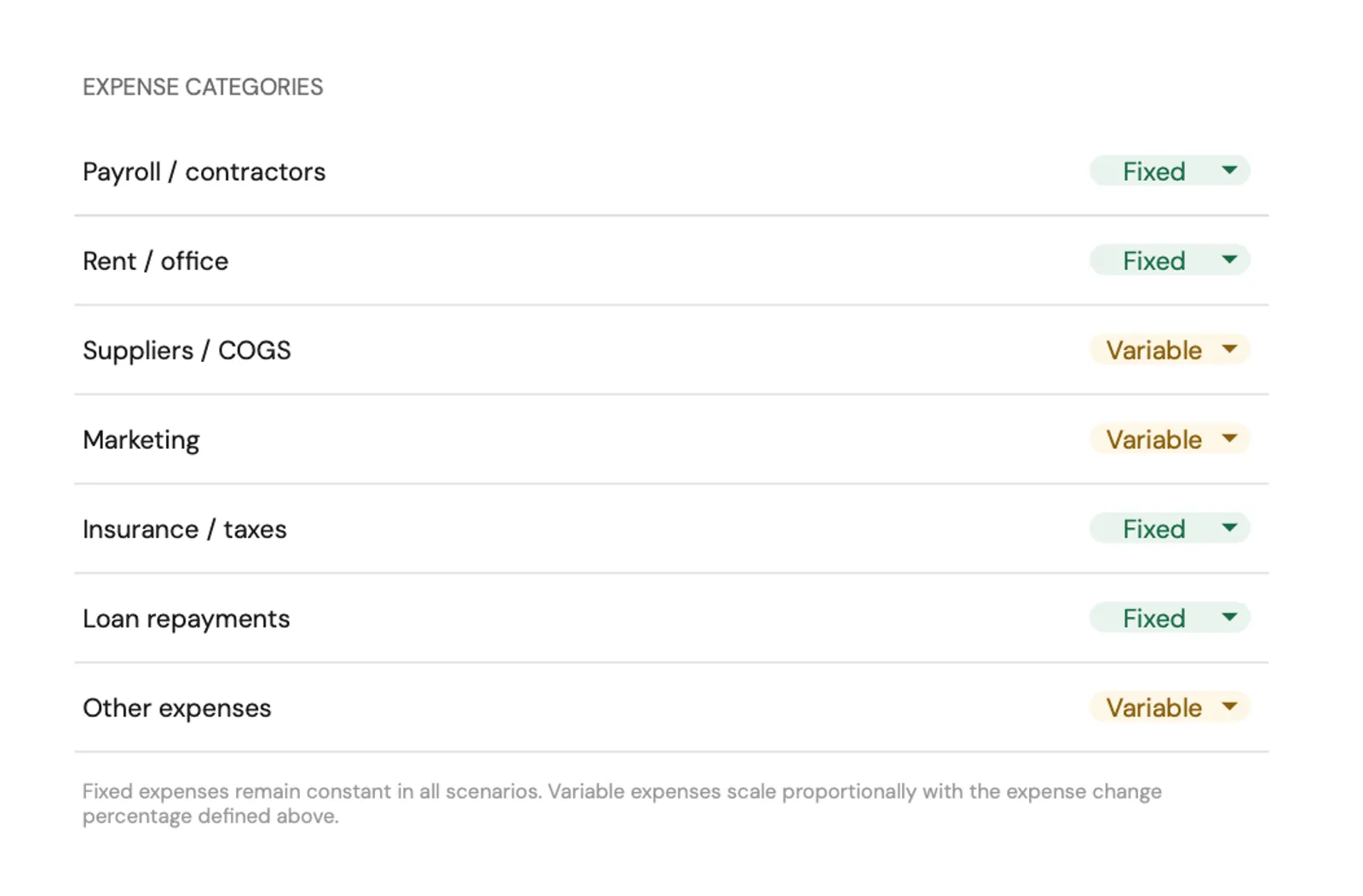

Set up expense categories for your business

Recommended Templates

Templates for Small Business Budgeting

Built for business financial management - forecast cash flow, track revenue and expenses, and plan for growth. See projected cash positions months ahead to avoid shortfalls.

View templateTrack business income, deductions, and estimated quarterly tax payments. Organized tax tracking throughout the year makes tax season straightforward.

View template Save $91Get business and personal financial tools together. Manage the business cash flow while keeping personal finances, retirement planning, and net worth tracking in order.

Includes 8 templates

View bundleFree Tools

Calculators to Help You Plan

Common Questions

Small Business Budgeting FAQ

How much should a small business budget for taxes?

Setting aside 25-35% of net profit covers federal and state income tax plus self-employment tax for most small businesses. The exact amount depends on business structure (sole proprietorship, LLC, S-Corp), income level, and state taxes. Working with an accountant to determine the right percentage is worth the cost.

What is the difference between a budget and a cash flow forecast?

A budget plans how much to spend in each category. A cash flow forecast shows when money actually comes in and goes out. A business might budget $10,000 for a project, but the cash flow shows that $5,000 is due upfront and $5,000 on delivery. Both tools serve different purposes.

How should new businesses budget with no revenue history?

Start with expense estimates (rent, supplies, marketing) and conservative revenue projections. Track actual numbers from day one and adjust the budget monthly as real data comes in. Most businesses find that initial budgets need significant revision in the first 6-12 months.

When should a business hire an accountant?

Most small businesses benefit from professional tax preparation from the start. As the business grows, monthly or quarterly bookkeeping support helps maintain accurate records. The cost of an accountant typically pays for itself through tax savings and avoiding costly mistakes.

How do seasonal businesses budget?

Seasonal businesses need an annual view that shows peak and slow months. Revenue earned during busy seasons needs to cover expenses during slow periods. Setting aside a portion of peak-season revenue specifically for off-season expenses prevents cash crunches.

Can't find the answer you're looking for? Contact our team

Start planning your small business budget

A spreadsheet template with automatic calculations, visual summaries, and everything needed to track small business costs.

Ready to get started?

Download instantly and start managing your finances, or contact us to design a custom template package for your needs.